Industry insider: the anticipated impact of the Cayman Islands' grey list removal on the CLO market

In this interview with Kareem Robinson, Head of Capital Markets at Ocorian in the Cayman Islands, we explore the potential implications of the jurisdiction’s expected removal from the Financial Action Task Force (FATF) grey list. As this significant development looms, we explore the likely shifts in the CLO (collateralised loan obligation) market in the Cayman Islands and its impact on European investors.

When was the Cayman Islands added to the FATF grey list and the EU AML blacklist?

The FATF placed the Cayman Islands on the grey list in February 2021 following the outcome of the jurisdiction’s mutual evaluation. At the time, the FATF acknowledged that the jurisdiction had met 60 out of 63 recommended actions. The three remaining actions to be addressed, before the Cayman Islands could be removed from the FATF grey list, were as follows:

- applying sanctions that are effective, proportionate, and dissuasive, and taking administrative penalties and enforcement actions against obliged entities to ensure that breaches are remediated effectively and in a timely manner.

- imposing adequate and effective sanctions in cases where relevant parties (including legal persons) do not file accurate, adequate, and up to date beneficial ownership information; and

- demonstrating that they are prosecuting all types of money laundering in line with the jurisdiction’s risk profile and that such prosecutions are resulting in the application of dissuasive, effective, and proportionate sanctions.

Following the grey listing, the Cayman Islands were subsequently added to the EU AML blacklist in March 2022. The list is made up of jurisdictions which the body deems to have strategic deficiencies in their Anti-Money-Laundering (AML) and Counter Terrorist Financing (CFT) regimes.

What were the implications on the CLO market when the Cayman Islands were added to the EU AML blacklist?

The Cayman Islands’ addition to the EU AML blacklist did not affect US CLO managers with Cayman Islands-issued securitisations who were solely seeking US investors. It did however impact managers seeking EU investors to their transaction using Cayman Islands securitisation SPVs and triggered a migration of CLO SPVs to other jurisdictions. This was due to Article 4 of the EU Securitisation Regulation that prohibits the establishment of securitisation special purpose entities in countries listed on the EU AML blacklist.

How will the removal of the Cayman Islands from the FATF grey list affect the CLO market on the island?

With the Cayman Islands being on both the FATF grey list and the EU AML blacklist, European CLO managers and investors have been unable to participate in transactions involving Cayman Islands-domiciled vehicles issuing CLOs since February 2021. However, once the Cayman Islands is removed from the grey list and subsequent blacklist, this regulatory barrier will cease to exist. European investors and managers will have the green light to utilise Cayman Islands entities as issuers and invest in CLOs domiciled in the Cayman Islands.

How do you foresee the perception of the Cayman Islands based CLOs changing among international investors, if the jurisdiction is no longer on the FATF grey list?

Since the grey listing, CLOs managed by US and European based CLO managers with EU investors have been domiciled in other offshore jurisdictions such as Jersey and Bermuda, however, once the restrictions are lifted, many CLO managers are expected to return to the Cayman Islands. The Cayman Islands has a well-established history and track record as a jurisdiction of choice for the formation of CLO issuers. Although some existing deals may stay in other jurisdictions for logistical reasons, new deals are likely to be done through the Cayman Islands, reinstating its status as a prime destination for CLOs.

What opportunities and challenges do you anticipate for CLO managers and their ability to attract new investors into Cayman Islands based CLOs?

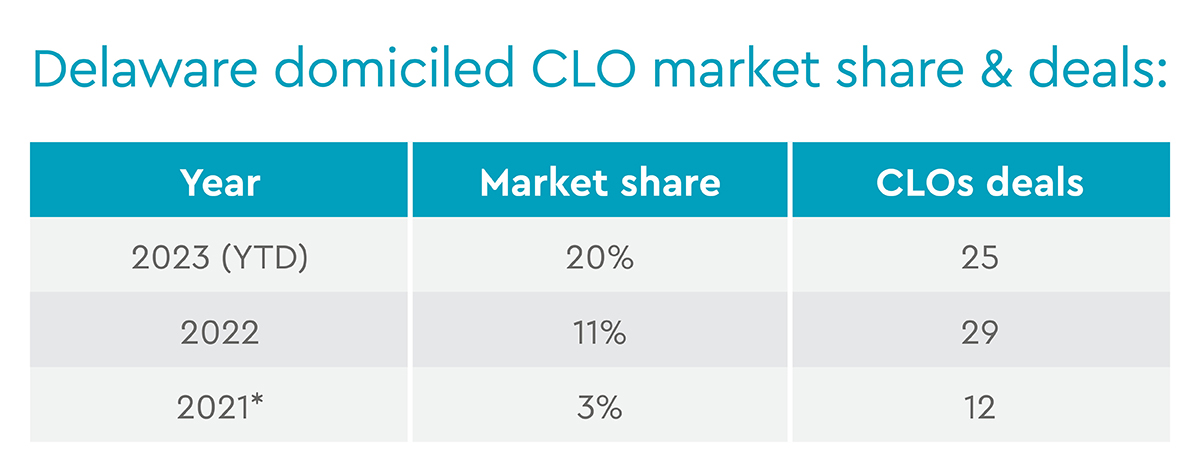

While the Cayman Islands' anticipated removal from the grey list is a positive development – this is the first step to being removed from the EU AML blacklist and it raises questions about the historical dominance of the jurisdiction. Some CLO managers turned to Delaware during the EU AML blacklisting period. Although the Cayman Islands is expected to regain prominence, Delaware's emergence as an alternative jurisdiction could pose future competition and should be watched closely.

Delaware domiciles CLO market share & deals:

* Information in 2021 was not as detailed as 2022 and 2023 but this figure points strongly to Delaware.

Even with Delaware’s growing popularity, the Cayman Islands still offers many benefits for most CLO managers and arrangers, such as the tax neutrality, legal certainty and the flexibility required to make CLOs tax efficient and operationally viable. Vehicles can be set up quickly and easily with the Cayman Islands’ simplified due diligence procedures and established infrastructure, and no form of corporate tax or duty is payable by a CLO noteholder on the issue, transfer or sale of notes. There’s an abundance of sophisticated local expertise to make even the most complex cross-border transaction run smoothly, making it an attractive option.

Are there any specific strategies or preparations that CLO issuers in the Cayman Islands should consider in anticipation of the jurisdiction's potential removal from the grey list, especially in the context of investor relations and market positioning?

CLOs previously domiciled or migrated to Bermuda and Jersey would likely remain, as it would be an onerous and costly process to migrate them back to the Cayman Islands with not much upside or benefit.

For new CLOs however, it is the expectation that CLO managers and European investors will transition back to the Cayman Islands. The history and familiarity with such structures, coupled with the ease of doing business, will make this transition seamless. The Cayman Islands' straightforward but robust regulatory environment, along with the relatively low-risk nature of CLOs, simplifies the operational process, and CSPs (Corporate Services Providers) like Ocorian anticipate a smooth and welcomed resurgence.

How will Ocorian navigate the Cayman Islands potential delisting from the FATF grey list and subsequent EU AML blacklist?

Ocorian will continue to work closely with its partners, ensuring a seamless transition to “business as usual” for existing clients and a consistent and value-added experience for new ones. Despite the challenges of jurisdictional competition, the strong reputation of the Cayman Islands in the CLO market is expected to endure, reaffirming its position as a trusted and reliable domicile for CLO issuers.

The Cayman Islands' potential removal from the FATF grey list and EU AML blacklist represents a pivotal moment for the CLO market. While challenges may arise, the historical strength and reputation of the Cayman Islands are expected to prevail, offering stability and opportunity to CLO managers and investors alike.

How can Ocorian help?

CLOs have become more intricate than ever, requiring specialised support throughout their lifecycle. Ocorian offers experienced teams in the Americas and Europe, providing comprehensive assistance from setup to liquidation across multiple jurisdictions.

Our global team based in the Cayman Islands, UK, Ireland, Jersey and Luxembourg are able to provide a seamless, cross-border client solution for CLOs spanning multiple jurisdictions.

Related Items

View all