Global public and private market assets surged £7.8 trillion in January and February 2025 but have given up almost half their gains in March

- Global assets jumped by $7.8 trillion in January and February, up 3.2% to a record $250.6 trillion by the end of February

- But US trade wars have caused a $3.4 trillion slump in March, mainly affecting US equities, leaving the global asset total up 1.8% year-to-date

- Equity markets are down $4.0 trillion in March - tumbling US share prices accounted for 93% of this decline

- Europe, Hong Kong, China and the UK made a strong positive contribution in 2025 – all seeing higher year-to-date equity values

- Bond markets have grown in 2025 owing to newly issued bonds

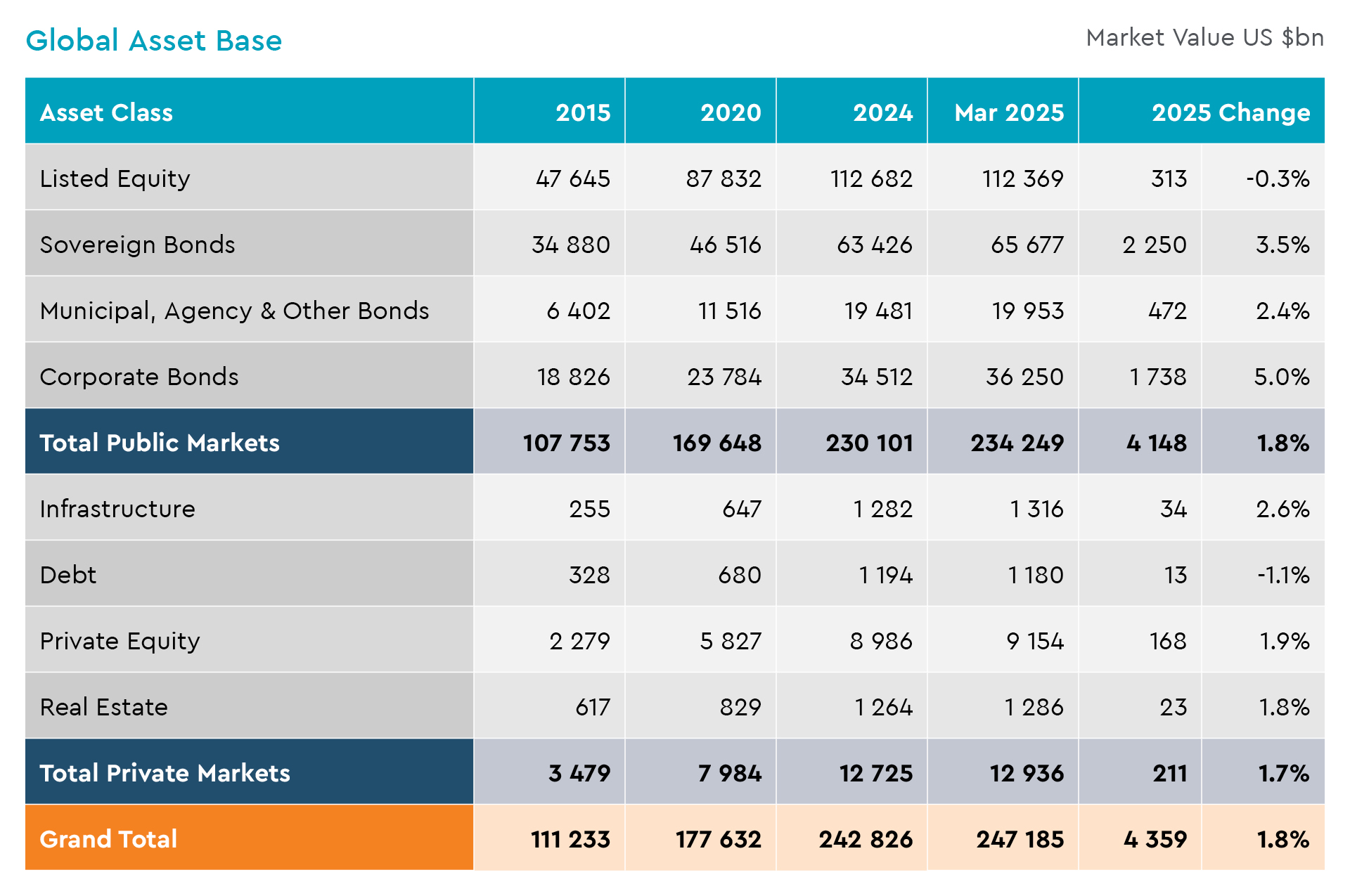

- Private markets are up 1.7% year-to-date to $12.9 trillion, mainly driven by private equity

- UK listed assets are up $354bn thanks to higher equity values, larger bond markets and a stronger currency

The value of the world’s assets surged ahead in the first two months of 2025, but in March alone have already given up almost half their gains, shrinking by $3.4 trillion, according to the latest Global Asset Monitor from Ocorian, a market leader in asset servicing for private markets and corporate and fiduciary administration.

Strong start to 2025

Between the New Year and the end of February, the main investable public and private asset classes (listed equities and listed bonds, and private funds investing private equity, private debt, real estate and infrastructure) – expanded by an astonishing $7.8 trillion. The 3.2% increase to a record $250.6 trillion by the end of February reflected strong equity markets and new borrowing by governments and companies on the bond markets, as well as expansion in private asset classes.

March – the impact of US trade wars

The sharp decline in March is driven almost entirely by US equities. Globally, the value of listed companies has fallen $4.0 trillion, 93% of which reflected shrinking US company values. Bond markets, by contrast, are $985bn larger. Private assets have declined, however, down an estimated $326bn since the end of February, driven mainly by lower private equity values.

The world’s assets were worth $247.2 trillion by 12th March 2025, up 1.8% year-to-date.

Image

US markets have borne the brunt of US trade policy – capital flight to Europe, UK and parts of Asia

Listed equity markets comprise almost half (46%) of the world’s investable assets. Donald Trump’s trade war has disproportionately hit US stocks, but many other markets have been more resilient. By the middle of March global listed companies had lost $313bn of value year-to-date, reflecting falling US share prices ($2.3 trillion lower). Most other regions are ahead year-to-date – European equities excluding the UK are $1.4 trillion more valuable, while UK stocks have added $193bn, reflecting higher share prices and a weaker dollar. Asian equities are up $218bn, driven by China and Hong Kong. India, Japan and Taiwan have all shrunk year-to-date.

Bond issuance means larger bond markets

The market value of the world’s bonds has increased $4.5 trillion year-to-date, up 3.8%. This mainly reflects new issuance and a weakening US dollar.

Private assets up 1.7% year-to-date

Private markets are smaller but they have made a growing contribution to the world’s asset base. Ocorian’s modelling of Preqin data suggests that private assets are 1.7% larger year-to-date, driven mainly by growth in private equity (especially in Europe and the US) and recovering real estate markets. Ocorian puts the value of private asset funds at a $12.9 trillion in March, up $211bn since the end of 2024, though this is slightly lower than the record peak reached at the end of February ($13.3 trillion).

Over the longer term, private assets have grown significantly faster than public markets. Private asset funds under management are almost 7.7x larger than in 2009 (+656%) compared to public markets 3.3x larger.

UK spotlight: The UK’s listed assets rose $338bn in January and February to a record $7.5 trillion, up 4.8%, outstripping the global average. Three fifths of this was due to rising UK share prices. The rest came from bond markets in a mix of new issuance and price changes, with a small contribution from a slightly stronger pound. In March, UK assets expanded very modestly as lower share and gilt prices were offset by a larger corporate bond market and the stronger pound.

Jason Gerlis, Head of Americas and Global Head of Corporate Services at Ocorian said: “Asset prices have whipsawed in 2025 in the face of concerns over government finances and the inflationary impact of US trade wars. But it’s US assets that are feeling the most pain, as a flood of capital out of US equity markets is washing up on shores in Europe and parts of Asia. Six of the US Magnificent 7 stocks have lost $2.3trillion of value since the New Year. This highlights how important diversification is. The growing concentration of stock market value in the US and among a few companies – the fifteen largest companies account for one fifth of the global total – is increasing risks for investors.

“Private markets can help investors achieve this much needed diversification. Private capital is transforming the way businesses grow. Public markets have long provided a structured path for companies to raise capital and investors to earn returns, but their reach is far more limited than their size suggests. And the vast majority of companies are still privately owned – around 90% in the US for example. Investors and businesses alike are seeking alternative paths to growth, and private capital is increasingly the bridge between opportunity and execution. The global investment landscape is shifting rapidly – the dramatic growth in private assets reflects both a flow of capital to the sector and superior performance over the long term.”

[1] Market close March 11th 2025

Related Articles

View all