Where should you domicile your alternative investment fund in Europe?

Choosing your alternative investment fund’s (AIF) domicile in Europe will depend to a large extent on your potential investor base, but that’s not the only consideration.

Other factors to take into account include the robustness and flexibility of local laws and tax arrangements, the maturity of the local service provider ecosystem and the ease of doing business.

In this article, we answer frequently asked questions about where to domicile your fund in Europe.

1. Should you domicile an AIF offshore or in the EU?

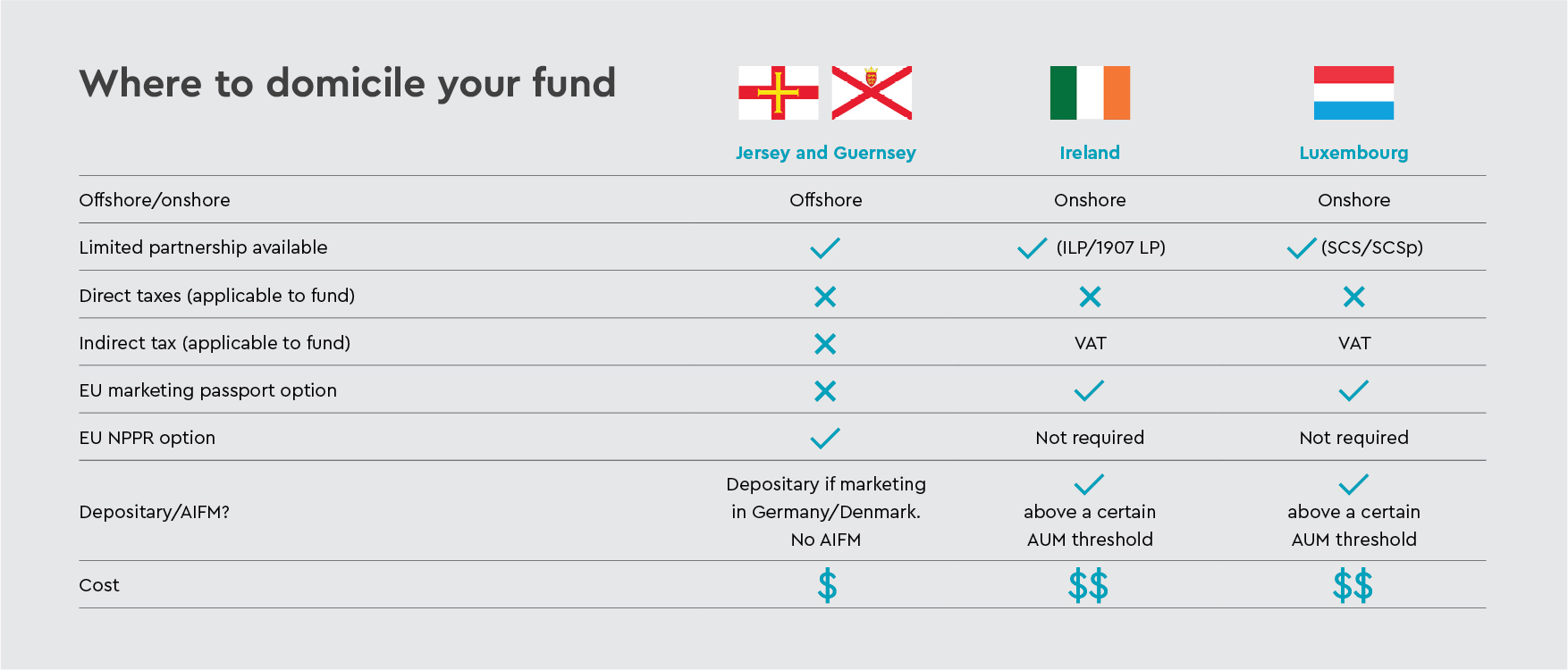

For overseas managers looking for the most complete access to European investors, the choice tends to come down to Luxembourg or Ireland. These EU jurisdictions bring the fund under the full scope of the EU regulatory regime, which can add administrative complexity. The upside is that EU-domiciled funds offer greater flexibility and the option to efficiently market the fund under the EU marketing passport.

Alternative asset managers can also choose to domicile the fund offshore, typically in the Channel Islands (Jersey or Guernsey), the Cayman Islands or the US. This allows them to take advantage of simpler regulatory environments, local tax incentives and potentially lower set-up and maintenance costs, but it adds cost and complexity to pan-European marketing, which has to be carried out on a country-by-country basis using NPPR. It also limits access to certain major investors, notably regulated institutional investors tend to shy away from offshore jurisdictions.

Fund domiciles in Europe

2. Are you familiar with the jurisdiction?

Having already domiciled a fund in one jurisdiction without too many problems, you’re more likely to do so again. This makes sense. You could mix and match, but why add another set of compliance requirements to your administrative burden? In addition, investors may have their own reasons for favouring one location over another.

3. What are the available fund structures in Europe?

Ireland

In Ireland, funds are established under either the Undertakings for the Collective Investment in Transferable Securities (UCITS) regime or as an AIF. UCITS are open ended and liquid funds aimed at retail investors. AIFs are covered by AIFMD and can involve a wider range of assets and investor groups. For real assets, the Qualifying Investor AIF (QIAIF) is the most popular AIF in Ireland, while the Retail Investor AIF (RIAIF) is aimed at non-professional investors. Legal structures include:

-

Irish Collective Asset Management Vehicle (ICAV)

A corporate investment vehicle designed for funds that can be used for both UCITS and AIFs. Its main advantage is that, although a corporate structure, ICAV legislation omits general company law provisions that are inappropriate for funds, making it simpler to administer. It can also be treated as a partnership for US tax purposes.

- Investment Limited Partnership (ILP)

An ILP can only be established as an AIF and does not have an independent legal existence. It is formed by agreement between one or more General Partners (GPs) and one or more Limited Partners (LPs). The GP is responsible for the management, control and operation of the ILP. ILPs are very similar to the limited partnerships many US managers will be familiar with.

Luxembourg

In Luxembourg, funds are also established as either UCITS or AIFs. Luxembourg equivalents of the Irish QIAIF include the Special Investment Fund (SIF) and the Reserved Alternative Investment Fund (RAIF). The main difference between the two is the level of regulatory supervision: while the SIF is directly regulated by the Luxembourg financial sector regulator (CSSF), the RAIF is only indirectly regulated through its requirement to appoint a regulated AIFM and Depositary, thus enabling a much shorter time-to-market.

In Luxembourg, the SCS and SCSp are similar to the ILP. Both are limited partnership structures, though only the SCSp does not have a legal personality. Both can be established as a SIF or RAIF or can remain unregulated.

In effect, there are regulatory frameworks and legal structures in both jurisdictions to meet the needs of overseas managers, and both offer limited partnership structures that are familiar to US-based funds.

4. How easy is it to do business?

GPs will look at factors like the taxation framework, the size and expertise of the local service provider ecosystem, and the cost and time to market of preferred vehicles.

The EU’s two main onshore domiciles largely mirror one another in these respects, though Luxembourg is considered the more established jurisdiction for AIFs with focus on real assets such as private equity, venture capital, private debt, infrastructure and real estate. The political and financial stability (AAA rating) of Luxembourg is frequently mentioned as well. Ireland has its own advantages, like a marginally more US-friendly time zone and – for some UK and US managers especially – a closer cultural fit. Jersey and Guernsey have similar advantages if an off-shore jurisdiction is required.

5. Are there any investor red lines?

Some major institutional investors in Europe can only invest in EU-domiciled funds. Others may choose to. Again, it’s crucial to research your distribution strategy and the priorities of your potential investor base before making a decision on your fund domicile.

Ocorian Fund Services

At Ocorian we have extensive experience supporting US fund managers with setting up alternative investment funds in Europe and administering them throughout their lifecycle.

We have teams across seven jurisdictions in Europe that provide a high touch, technology first approach combined with local expertise.

We offer a full service offering from fund set up and administration through to fund accounting, AIFM, investor services and depositary.

- Fast and efficient set up of funds in Europe

- Teams based in the UK, Jersey, Guernsey, Ireland, The Netherlands and Luxembourg

- AIFM in Ireland and Luxembourg

- Expertise in administering vehicles parallel to existing US or Cayman structures

- Jurisdiction agnostic

- Full service provider

Our business development team in the US will be happy to discuss your European requirements and guide you through the process. Contact us for more information.

Download ‘A guide to setting up your fund in Europe’

Fill in the form to download your free guide of ‘How to set up a fund in Europe’.

Related Items

View all