How to establish a QIAIF in Ireland

Ireland stands as a premier global hub for alternative investment funds (AIFs), attracting fund managers and investors worldwide with its favourable regulatory and tax environment.

In this article, Stephen Hickey, Eamon Burns and Eileen McCarroll from Ocorian’s Fund Services Team in Ireland delve into the specifics of establishing a Qualifying Investor Alternative Investment Fund (QIAIF) in Ireland – a vehicle designed for sophisticated investors seeking flexible, efficient, and strategic investment opportunities.

Introduced in 1990, QIAIFs have set the standard in Europe for regulated alternative investment products, offering a broad array of strategies from private equity and real estate to hedge funds and venture capital.

Here, we explore the key features, benefits, and procedural steps involved in setting up a QIAIF, highlighting why Ireland continues to be the jurisdiction of choice for alternative investments.

What is a QIAIF?

QIAIF stands for Qualifying Investor Alternative Investment Fund. It's a type of regulated investment fund established in Ireland specifically for institutional investors, high-net-worth individuals, and other qualified investors.

Ireland was the first European jurisdiction to offer a regulated alternative investor fund product – the Irish Qualifying Investor Alternative Investment Fund (QIAIF) – in 1990.

QIAIFs are established in compliance with the Alternative Investment Fund Managers Directive (AIFMD) and cover a broad range of alternative investment strategies, including private equity, real estate, fund of funds, venture capital and infrastructure.

What are the features of a QIAIF?

- Regulated: QIAIFs are authorised and overseen by the Central Bank of Ireland, ensuring a level of security and transparency for investors.

- Targeted investors: These funds target qualified investors who meet specific criteria, typically with a minimum investment threshold of €100,000.

- Investment flexibility: QIAIFs offer a high degree of flexibility in terms of investment strategies and asset types. They can be used for various investment approaches, including private equity, real estate, hedge funds, and more.

- AIFMD compliant: QIAIFs comply with the European Union's Alternative Investment Fund Managers Directive (AIFMD), which sets standards for managing alternative investment funds across Europe.

- Fund manager: A QIAIF must appoint an Alternative Investment Fund Manager (AIFM), which can be either an EU-based or non-EU manager responsible for overseeing the fund's operations.

What are the benefits of establishing a QIAIF in Ireland?

- EU access: QIAIFs benefit from the EU marketing passport. This allows them to market to professional investors throughout the European Union if they are authorised under the AIFMD.

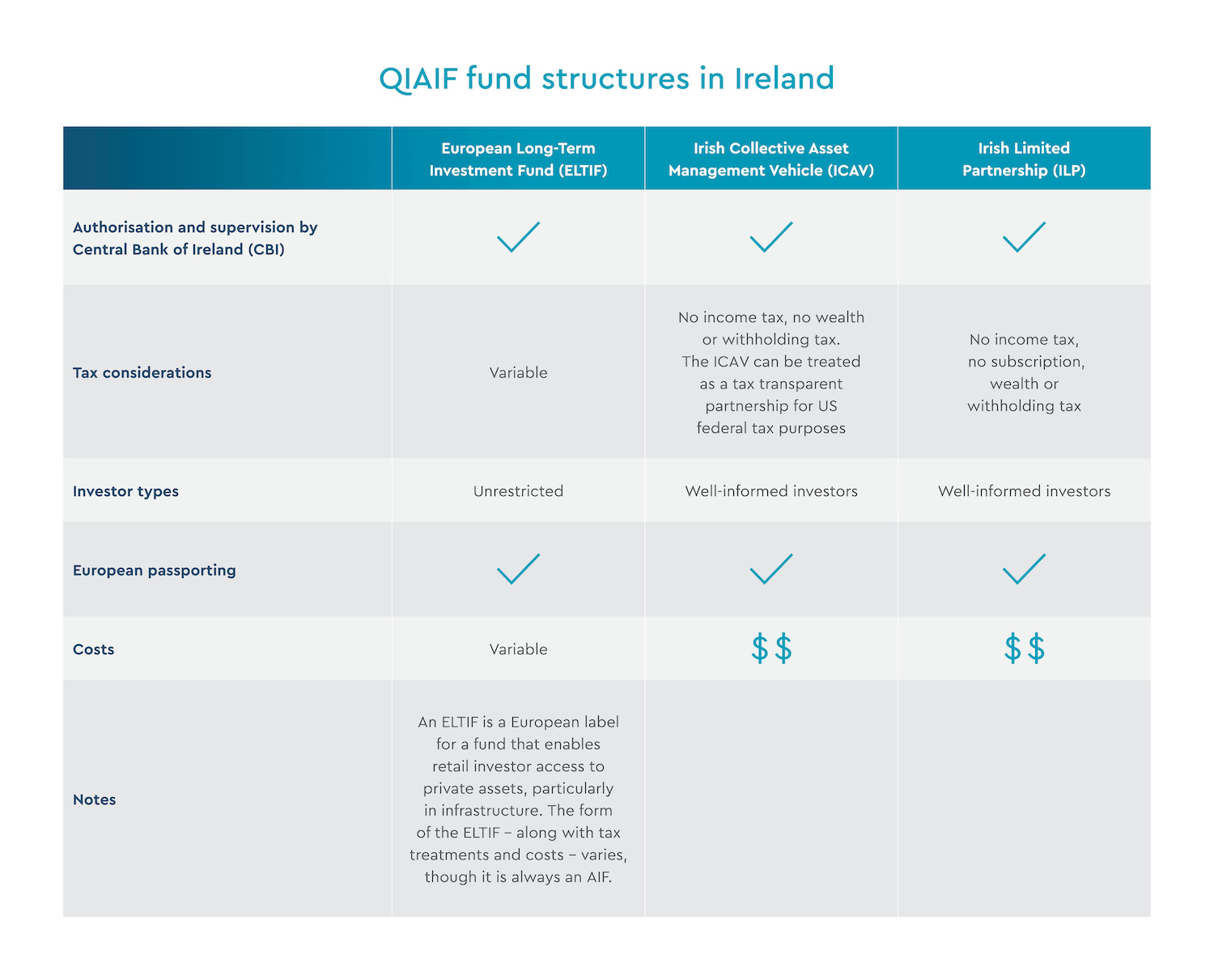

- Flexible fund structures: QIAIFs offer a variety of legal structures to choose from, including Irish Collective Asset-Management Vehicles (ICAVs), Common Contractual Funds (CCFs), Open-ended Unit Trusts, Investment Companies/Variable Capital Companies, and Investment Limited Partnerships (ILPs). This flexibility ensures managers can select the structure that best suits their needs.

- Re-domiciliation friendly: Existing investment funds from other jurisdictions can be re-registered in Ireland through a process called re-domiciliation.

- Fast launch: QIAIFs can be established quickly, typically within 10-16 weeks, when using an authorised AIFM. The Central Bank of Ireland offers a swift 24-hour approval process upon receiving complete documentation.

- Tax advantages: QIAIFs enjoy a favourable tax regime. They are exempt from Irish income and capital gains taxes, distributions to non-Irish investors are free of withholding taxes, and they benefit from a wide range of VAT exemptions on related services. Additionally, QIAIFs can leverage Ireland's extensive double taxation treaty network covering over 70 countries.

- Few investment restrictions: The principal ones being those imposed by AIFMD on certain private equity type strategies and on investments in securitisations and certain Central Bank of Ireland imposed restrictions.

- No borrowing or leverage restrictions: Other than for loan origination funds.

- Listing opportunities: Listing on the Irish Stock Exchange is readily available, if desired.

- Migrate offshore funds: There is capacity to migrate offshore funds from a number of domiciles to Ireland as QIAIFs, via a reasonably efficient process, avoiding any asset realisation.

What is the structure of a QIAIF?

What legal structures are available for QIAIFs?

- Irish Collective Asset Management Vehicle (ICAV): This is a popular corporate structure for AIFs. It offers several advantages:

- Simpler administration: ICAV legislation excludes irrelevant company law provisions, making it more efficient to manage.

- Tax benefits: It can be treated as a partnership for US tax purposes in certain cases.

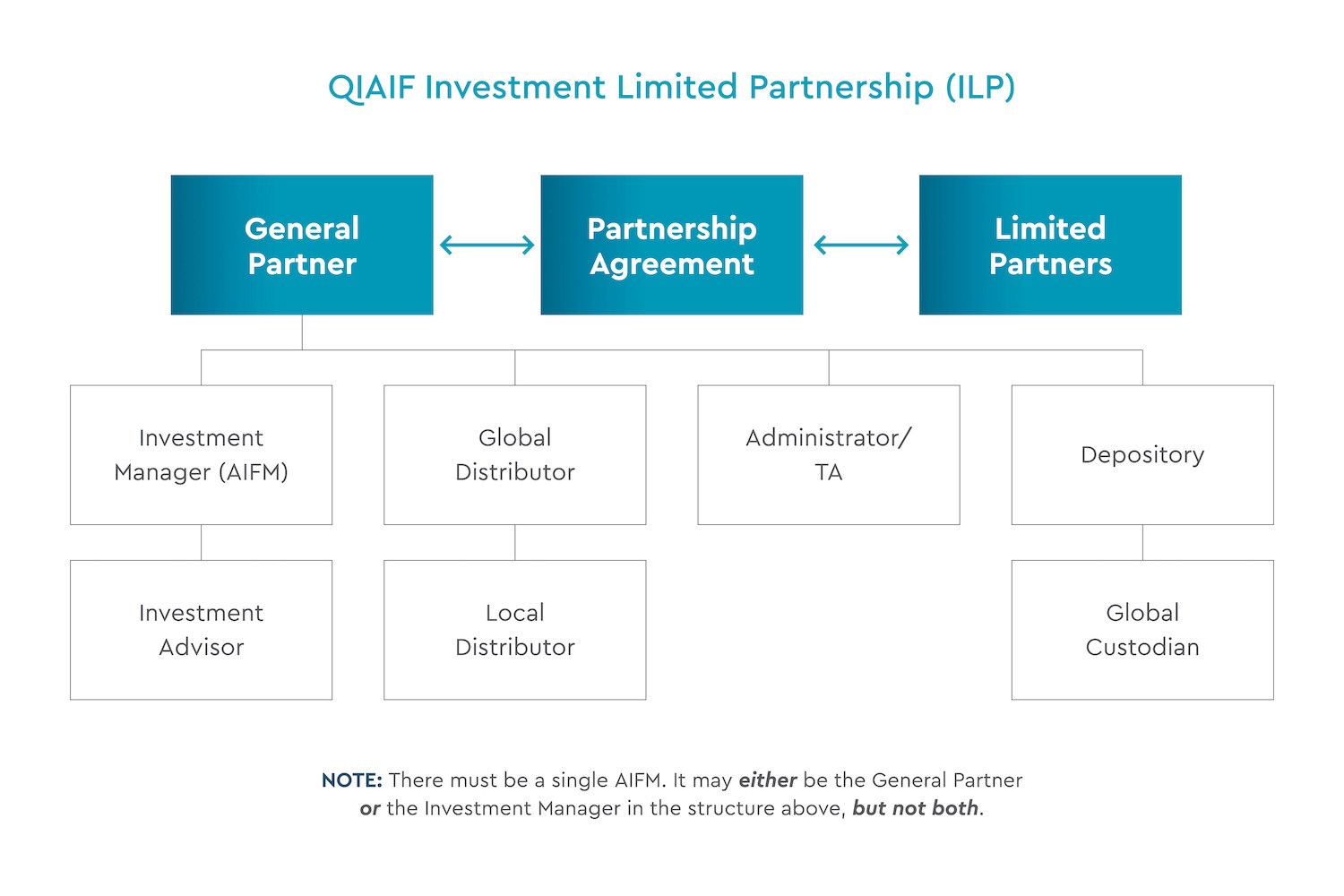

- Investment Limited Partnership (ILP): This structure can only be used for AIFs. It's similar to limited partnerships in the US and involves:

- General Partners (GPs): Responsible for managing and controlling the ILP.

- Limited Partners (LPs): Contribute capital but have limited involvement in management.

When it comes to real estate investment structures in the US, real estate managers overwhelmingly choose the ICAV structure for their funds, whereas the ILP is more commonly used for private equity and venture capital investments.

What are the features of an ICAV (QIAIF)?

An ICAV stands for Irish Collective Asset-Management Vehicle. It's a popular legal structure used to establish investment funds in Ireland.

- Corporate structure: An ICAV is a separate legal entity with its own board of directors, similar to a company. This structure offers advantages like limited liability for investors.

- Fund flexibility: ICAVs can be established as either open-ended or closed-ended funds. Open-ended funds allow for ongoing investor participation, while closed-ended ones have a fixed number of shares offered at launch.

- UCITS & AIFs: ICAVs can be used for both UCITS (Undertakings for Collective Investment in Transferable Securities) and AIFs (Alternative Investment Funds), catering to a wide range of investment strategies.

- Modernised framework: Compared to older fund structures, ICAVs have a more streamlined legal framework designed specifically for investment funds. This can reduce administrative burdens and costs.

- Tax advantages: ICAVs can be particularly attractive for US investors due to their "eligible entity" status for US tax purposes. They are typically used by real estate asset managers.

Why is the ILP (QIAIF) an attractive proposition for asset managers?

Before the introduction of the Irish Investment Limited Partnership (ILP) regime, Luxembourg held a dominant position in attracting private market funds, particularly those from the US. Ireland, on the other hand, had a strong presence in the public markets, especially with hedge funds. The Irish government, however, recognised the potential of the private markets and has recently focused on this area.

In 2020, Ireland modernised its investment fund framework with the Investment Limited Partnerships (Amendment) Act. This act created a new, internationally competitive structure called the Irish Limited Partnership (ILP).

The ILP is designed to meet the needs of private equity firms and caters to a wide range of investment strategies, including real estate, venture capital, and infrastructure. Unlike some other structures, ILPs are not subject to legal risk spreading obligations, making them suitable for funds with concentrated holdings.

The ILP makes Ireland even more attractive for private investment funds, not only for new business but also established managers from other jurisdictions looking to relocate. This structure offers US managers a compelling alternative to Luxembourg for their European private market funds. In addition to being a regulated LP structure, the ILP allows for pan-European marketing and distribution.

The ILP's flexibility allows for the creation of multiple sub-funds under one umbrella, making it a cost-effective solution for managers with diverse investment strategies.

The key features of an ILP:

- Regulated structure: The ILP is a regulated EU AIF.

- Cost-effective structure: The ILP allows for creating multiple sub-funds under one umbrella, reducing costs compared to setting up individual vehicles for each investment strategy.

- Attractive to new and established managers: The supportive regulatory environment encourages both new fund formations and relocations of existing managers from other jurisdictions.

- Benefits for sophisticated investors: The ILP facilitates investments in sustainable projects like infrastructure, green energy, and social housing, appealing to pension funds and other socially conscious investors.

- Access to European markets: The ILP structure allows private equity firms to establish parallel European structures for their offshore funds, enabling distribution to European investors through the AIFMD passport.

- Commercially viable model: The ILP offers a fit-for-purpose and commercially attractive partnership model for private equity and other asset classes requiring tax transparency.

- Appeals to institutional investors: Regulation by the Central Bank of Ireland and adherence to international best practices make the ILP a secure and trustworthy option for institutional investors.

- Strong option for private equity: Ireland's reputation and the ILP's features make it a compelling choice for private equity managers. It offers standard private equity/real assets fund features including but not limited to:

- closed-ended/finite life

- capital accounting commitments, capital contributions and drawdowns

- excuse and exclude provisions

- defaulting investor provisions

- distribution waterfalls and carried interest

- advisory committee

How to establish an Irish QIAIF

The Irish government and the Central Bank of Ireland (CBI) have streamlined the process for establishing a QIAIF, ensuring it's both attractive and adheres to the highest standards.

- Choose your legal structure: There are various structures available, each with unique benefits in areas like tax treatment, risk management, and demonstrating substance. The fund's purpose will determine the best structure for your needs.

- Appoint qualified service providers: QIAIFs work with a variety of service providers, including administrators, depositaries, AIFMs, auditors, and directors. The CBI requires pre-approval of all providers to ensure competency. For instance, the AIFM, directors, and auditor must all be pre-cleared. Interestingly, while the administrator and depositary must be separate legal entities, they can be part of the same corporate group.

- Obtain regulatory approval: The CBI authorises and supervises all QIAIFs. The approval process depends on the chosen structure and selected providers. Only after all elements are in place will the CBI grant approval.

- Prepare necessary documentation: Comprehensive documentation is a must. If a management company is involved, it will need a Programme of Activity (POA) outlining its management functions, capital requirements, and monitoring procedures. Legal counsel will draft key documents like the prospectus, constitutive documents (e.g., instrument of incorporation for an ICAV), and agreements with service providers.

Ireland's QIAIF regime prioritises both a high-quality offering and strong regulatory standards. However, the CBI has ensured the process is straightforward, allowing investment managers to focus on attracting capital for their funds.

How can Ocorian help in Ireland?

Ocorian is licensed by the Central Bank of Ireland to provide fund administration, depositary and AIFM services to QIAIFs in Ireland.

Our team based in Dublin can support throughout the entire lifecycle of a fund for large-scale institutional investors, international fund promoters and investment managers across all investment structures.

Contact our fund services team for more information.

Download our free guide: Raising capital in Europe

Fill out the form below to receive your copy:

Related Items

View all