5 step guide for firms preparing for the sustainability disclosure requirements (SDR)

Following on from our summary of the FCA’s approach to standardising the UK’s market for sustainable investing, 2024 will see the majority of the regime rules come into force staggered May through to December.

All FCA regulated firms will be subject to the new anti-greenwashing rules and guidance from 31st May 2024, with more specific and onerous requirements targeting regulated asset managers.

Firms will be able to start labelling their products with accompanying disclosures from 31st July 2024, and the new naming and marketing rules will come into force on 2nd December 2024, again with accompanying disclosures.

To help you prepare for the new rules, we have outlined our 5-step approach to tackling them.

Whilst FCA regulated firms are caught by the anti-greenwashing rules, there are more detailed requirements for ‘in-scope firms’ and ‘in-scope products’ – particularly for those firms who choose to label their products.

In-scope firms are defined as:

- Full-Scope AIFMs;

- Small authorised UK AIFMs;

- UK Management Companies of UCITS; or

- Investment Companies with variable capital that is a UCITS scheme without a separate management company.

In-scope products are defined as:

- UK Authorised funds (UCITS and authorised AIFs); or

- Unauthorised UK AIFs including investment trusts.

Step 1: Preparing for the anti-greenwashing rules

Effective from May 31, 2024, the following rules apply to all communications and financial promotions directed at UK-based clients, whether made by or approved by an FCA-authorised entity. This pertains specifically to financial products or services that mention the sustainability characteristics of said products or services.

Sustainability-related references can be present, but a firm must ensure that any reference to sustainability characteristics[1] are consistent with the product or service and that all representations made a fair, clear and not misleading.

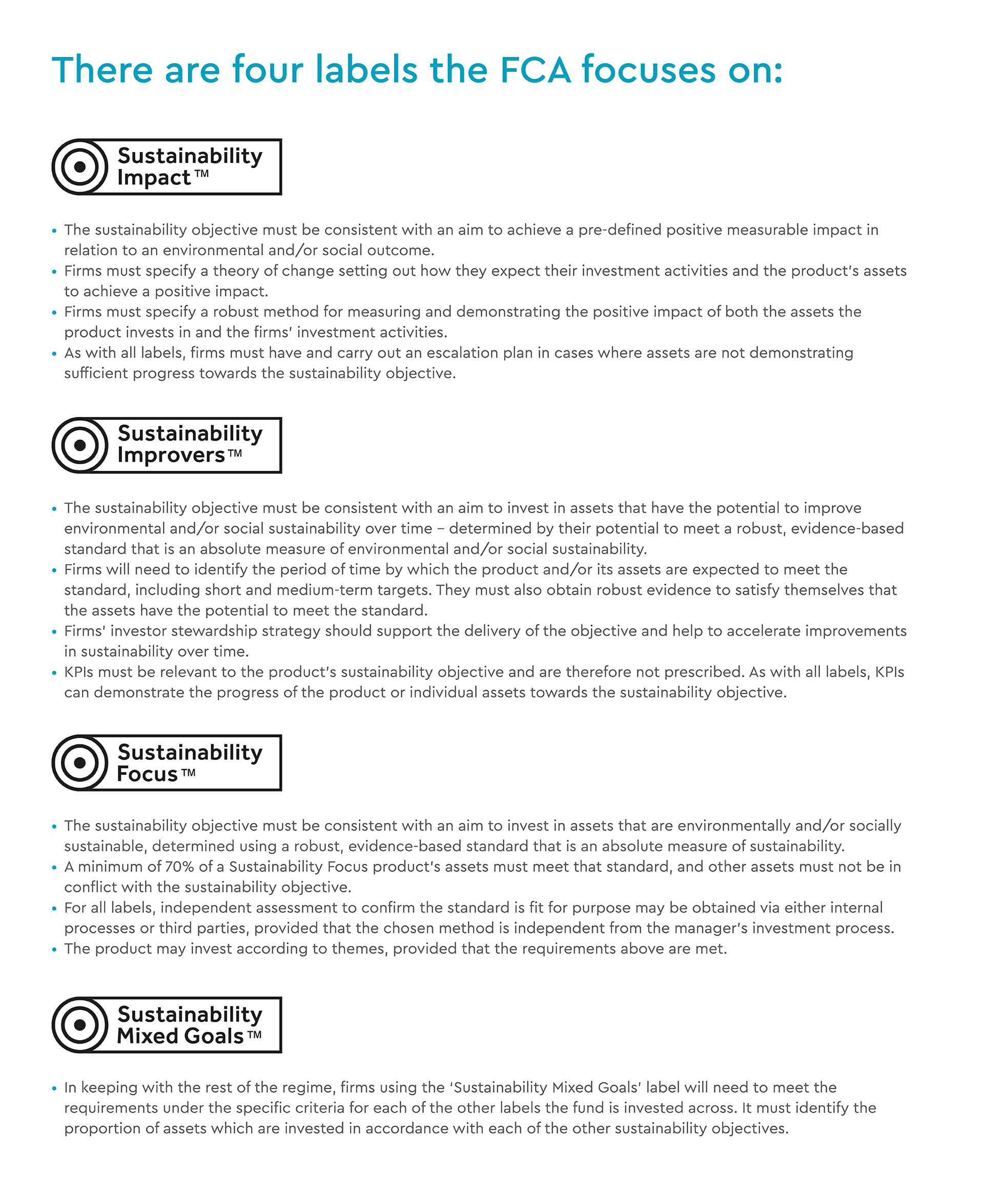

Step 2: Assessing ‘in-scope product’ labelling

Qualifying criteria to use an investment label:

1. Sustainable objective

A product with a statement of intention to undertake activities with the aim of directly or indirectly improving or pursuing positive environmental and/or social outcomes. The manager must also determine whether the product’s sustainability objective could result in negative environmental or social outcomes.

FCA guidance indicates that when a firm is determining its sustainability objective, it may wish to refer to the standards produced by the Sustainability Accounting Standards Board. This is because these standards can help firms to determine product or asset characteristics that retail investors might associate with sustainability.

2. Investment policy & strategy

The investment policy mandates that 70% of the product’s assets align with sustainability goals, directly or indirectly benefiting the environment or society. These assets must adhere to robust evidence-based standards. The remaining 30% of investments should avoid conflicting with the product’s sustainability objective. A systematic approach guides asset selection for the product.

3. Resources & governance

The resources and governance must match the product's ability to achieve its sustainability goal. The portfolio management team are required to have the necessary knowledge and understanding of the underlying assets and conduct a rigorous due-diligence process. The firm must ensure that an independent review is conducted by a qualified individual, (either internal or external) of the standard used by the portfolio management team to select the assets to invest in. The product is subject to at least an annual documented review and the manager must have an escalation plan in place if progress toward the sustainability objective is not being made as expected.

4. Stewardship

Stewardship can play a crucial role in accelerating the transition. However, the FCA have not been prescriptive in terms of requiring firms to demonstrate active engagement. Cross referencing to the UK Stewardship Code would adequately demonstrate the firm’s role.

Step 3: Choosing your investment label

In addition to general criteria, firms will be required to meet specific criteria dependent on the type of label chosen. The introduction of investment labels for products underpins the FCA’s approach to standardising responsible investing.

Step 4: Naming & marketing rules

Products that are made to retail investors and do not carry an investment label, must meet strict naming and marketing rules.

Product names

A product's name must accurately reflect its sustainability characteristics, but it cannot include the terms 'sustainable', 'sustainability', 'impact' or any variation of those terms.

Other terms that may be included in the name of a product that are synonymous with sustainability, for example 'net-zero', 'climate'; 'transition' or 'Paris-aligned', are detailed in ESG 4.3.2.

Firms must also produce and prominently publish a statement (on the relevant digital medium for the product and in the product-level disclosures) to clarify that the product does not have a label and the reasons why.

In the case of a feeder fund, the product must only include in its name terms which are consistent with those used by the relevant master fund and the asset manager must provide clients with easy access to the disclosures referred to above, and produce the relevant statement.

Marketing

Firms should be able to accurately describe their products so that consumers are able to navigate to those that meet their needs and preferences. The FCA understand that a blanket ban and restriction of specific terms in reality is not practical. Therefore, sustainability-related terms in their marketing are permissible if certain conditions are met.

As with the naming rules, the marketing rules only apply to products that use sustainability related terms made available to retail investors.

In the case of a feeder fund, firms must meet the same conditions as when sustainability-related terms are used in the name of the product.

Step 5: Disclosures

Our final step in preparing for the new SDR requirements, is determining the type and level of detail required in information disclosures.

Consumer-facing disclosures

Firms must produce a clear, concise consumer-facing disclosure for i) products with a label (ii) or products using sustainability-related terms without a label.

It must be in a prominent place on the relevant digital medium (e.g., webpage, mobile app) through which the product is offered, and hard copies must be made available on request and must not exceed two pages.

The disclosure must include the following information:

- either the product’s sustainability objective and label, or the statement to clarify that the product does not have a label;

- the investment policy and strategy (including what the product will and will not invest in);

- relevant metrics; – details of where a consumer can access other relevant sustainability and non-sustainability information; and

- for the ‘Sustainability Mixed Goals’ label only, the proportion of assets invested in accordance with each of the other relevant labels.

It must be reviewed and updated annually as appropriate. Disclosures for products with labels must, at a minimum, be updated to reflect progress towards achieving the sustainability objective.

Product-level disclosures

Product-level disclosures are aimed at institutional investors and retail investors who may want more information in either precontractual or in Part A of a sustainability product report, ongoing or Part B of a sustainability product report, on-demand disclosures are at the request of the investor.

All products using a label or using sustainability-related terms in their naming and/ or marketing without a label must include sustainability information in:

- Pre-contractual disclosures (from the date the label is first used or by 2 December 2024 for products using the terms without a label), and

- Ongoing product-level disclosures annually (after 12 months from either the date the label or terms are used)

For products using a label, the information that must be disclosed is broadly associated with the qualifying criteria for the labels.

For products not using a label, the pre-contractual and ongoing product-level disclosures must, at a minimum, include information relating to the investment policy and strategy and any relevant metrics.

For the ‘Sustainability Mixed Goals’ label only, the disclosures must include the proportion of assets invested in accordance with each of the relevant labels, and the information required in relation to those labels.

Entity-level disclosures

Consistent with the Task Force on Climate-related Financial Disclosures and International Sustainability Standards Board 4 pillars, firms are required to disclose their governance, strategy, risk management, metrics and targets in relation to managing sustainability-related risks and opportunities.

The TCFD’s supplementary guidance for asset managers, IFRS sustainability disclosure standard (IFRS S1), the SASB Standards and GRI Standards are documents that may be relevant for firms to help determine what to disclose.

Where firms use labels or sustainability-related terms in their product names and marketing, they must also include details on their resources, governance and organisational arrangements in relation to those products.

All firms with over £5 billion AUM must make these disclosures annually in a sustainability entity report, which builds from the TCFD entity report.

Firms can cross-refer to disclosures made in a group, parent-level or other relevant report, provided the information is clearly signposted and other cross-referencing requirements are met.

How can Newgate Compliance help?

If you require further assistance in meeting the new SDR requirements, please contact our Newgate Compliance team to ensure your firms readiness. We will work with you to develop a customised compliance plan that meets your specific needs, and we will be there to support you every step of the way.

[1] Sustainability characteristics defined by the FCA as environmental or social characteristics - https://www.handbook.fca.org.uk/handbook/glossary/G4650s.html

Related Items

View all