Global value of private assets held in funds rises 15.4% to another all-time high of $14.9 trillion

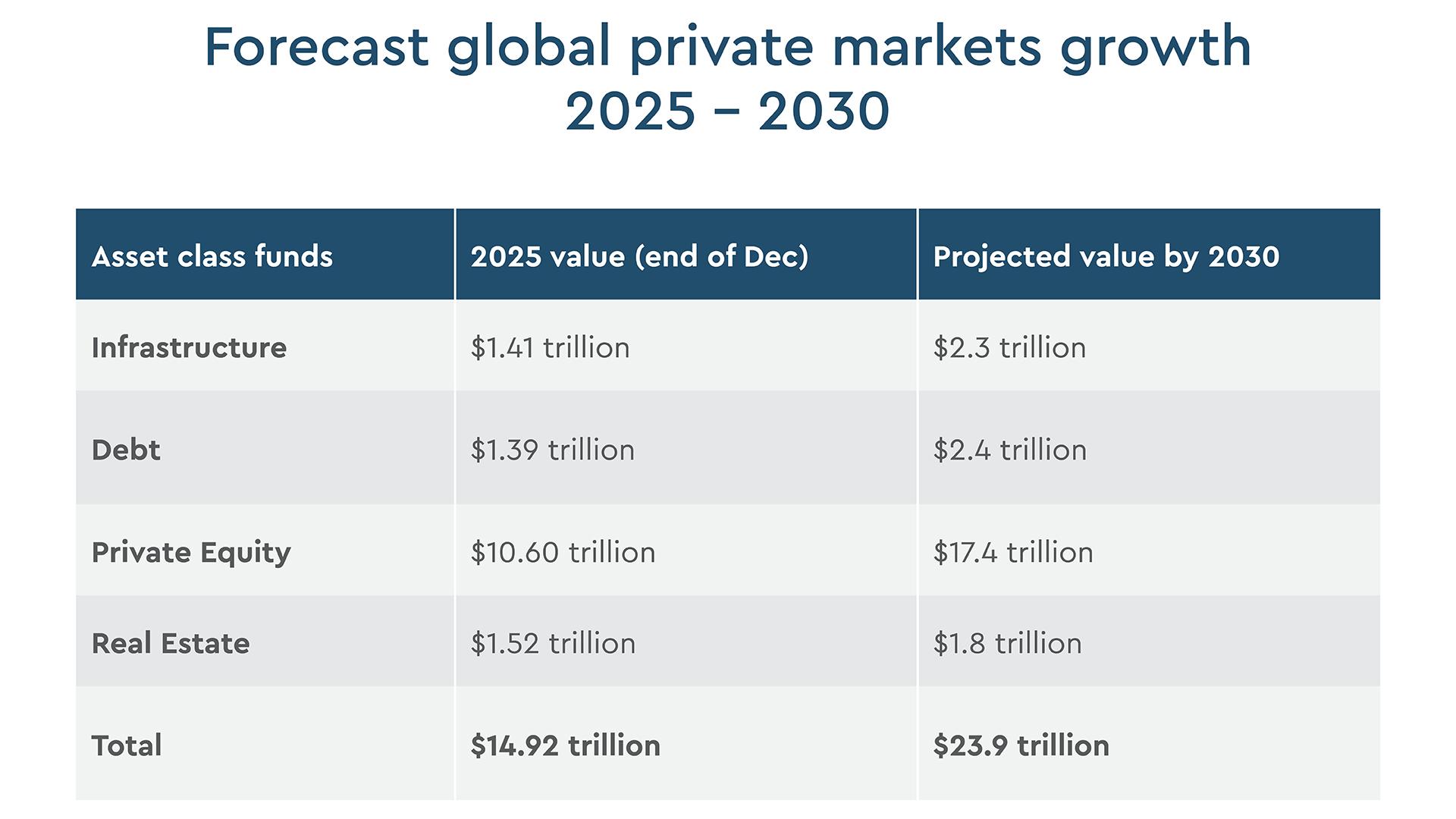

Ocorian’s Global Asset Monitor forecasts global value of private assets will hit record-breaking $23.9 trillion by 2030 with private equity rising by two thirds to $17.4 trillion

Middle East domiciled private markets reached record $73 billion, up from $64 billion, and Ocorian predicts these will double in the next five years

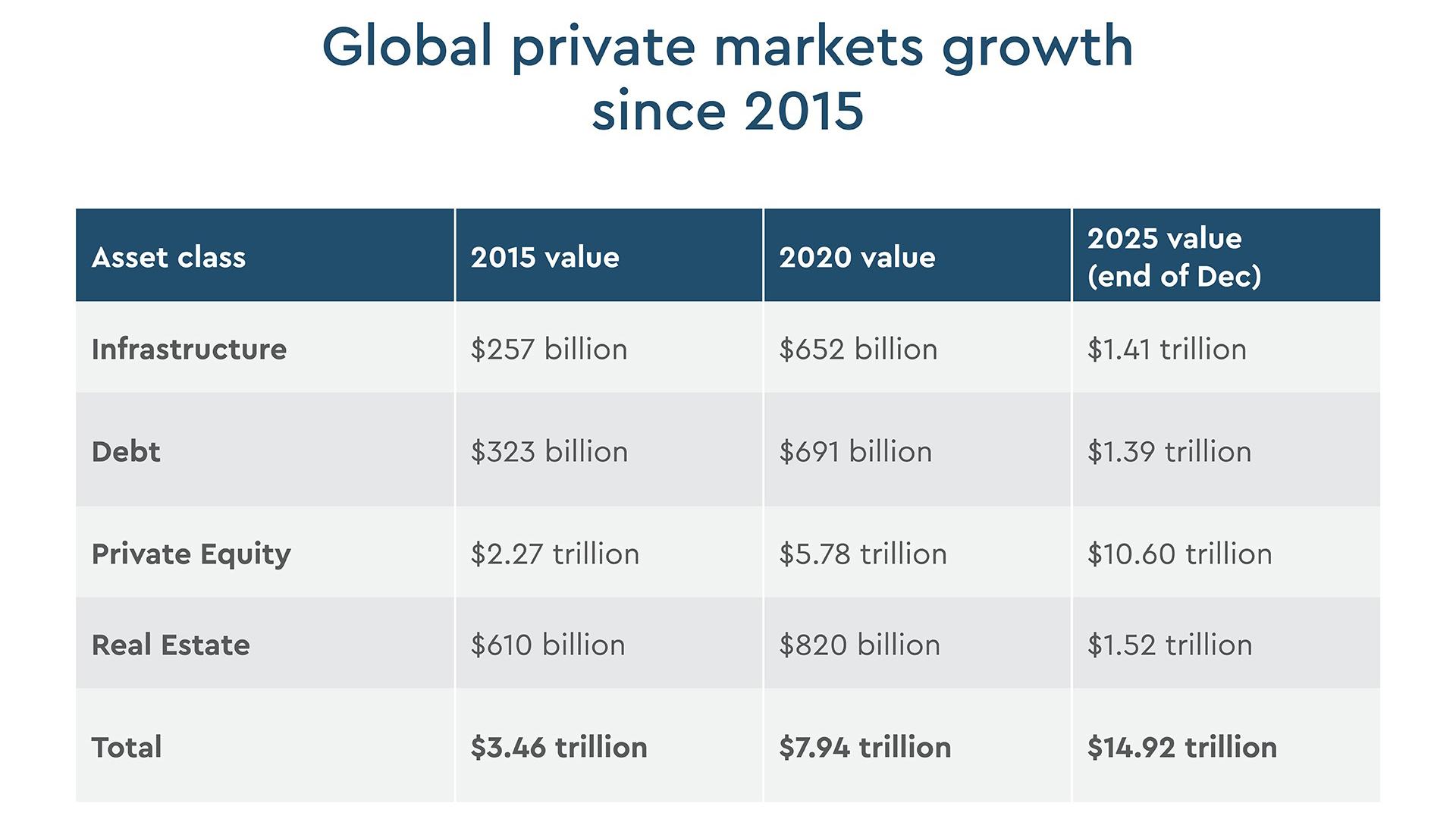

The value of global private assets funds surged to a record $14.9 trillion by the end of 2025, a 15.4% increase in the past year continuing the strong growth in the sector. The global value of private assets has surged by 87% since 2020, and 330% since 2015, and is forecast to climb another 60% by 2030 to hit $23.9 trillion. This is according to the latest Global Asset Monitor from Ocorian*, a market leader in asset servicing for private markets and corporate and fiduciary administration.

Global private equity fund asset values are driving the growth in private markets rising 17.8% in 2025 to a record $10.6 trillion at the start of this year – the highest annual growth rate since 2021. Ocorian’s Global Asset Monitor forecasts the total value of private equity assets will rise by two thirds to reach $17.4 trillion by the end of 2030.

Image

Growth of listed and private global assets

Ocorian's Global Asset Monitor, which analyses private market fund values as well as listed equities, sovereign bonds, corporate bonds and municipal agency and other bonds, estimates total global assets in 2025 experienced the largest annual increase ever recorded, up $38.6 trillion year-on-year (15.8%) to a record $282.9 trillion.

Within that total global private equity, private debt, infrastructure and real estate funds all hit record valuations and Ocorian forecasts growth will continue building on expansion over the past 10 years. However, it believes the growth in assets will drive consolidation with mainstream fund managers increasingly targeting the private markets sector.

Ocorian’s analysis shows 2025’s soaring growth in private equity global assets has been driven in particular by Asian markets which hit a record $2.4 trillion, up 28% year-on-year. Assets in North America still dominate fund holdings – Ocorian’s modelling shows they ended 2025 at $5.4 trillion, comprising of just over half of the world’s AUM. Funds based in Asia topped $3.2 trillion, double Europe’s $1.6 trillion and funds in the Middle East ended the year managing $55 billion.

Ben Hill, Global Co-Head of Fund Services at Ocorian said: "Our latest edition of the Global Asset Monitor reveals the record-breaking reality of private asset funds growth over the last year. The surge to £14.9 trillion during 2025 further supports our projection that private asset funds markets will expand to $23.9 trillion by the end of the decade, up 60% on today’s value.

“Private markets are growing while public markets remain constrained by rates, concentration risk and fewer viable exits. We see long-term growth across all four main asset classes.

“Key trends that will support the growth of private equity include the choice by companies to delay or avoid public listings when seeking an exit, resulting in private investors having access to value for longer. In the private credit space, borrowers value the speed and flexibility private lenders offer compared to traditional banks. Tailored debt structures and strong alignment with private equity sponsors often outweigh higher cost of capital for many borrowers. For infrastructure, patient capital suits long-term project finance, while private real estate funds provide far greater flexibility than public REITs meeting the needs of investors, developers and property operators.

“At Ocorian, we help alternative asset managers handle operational and regulatory complexity across the full investment lifecycle, especially when operating scale is a differentiator and investor profiles along with their needs are evolving fast across asset classes."

Image

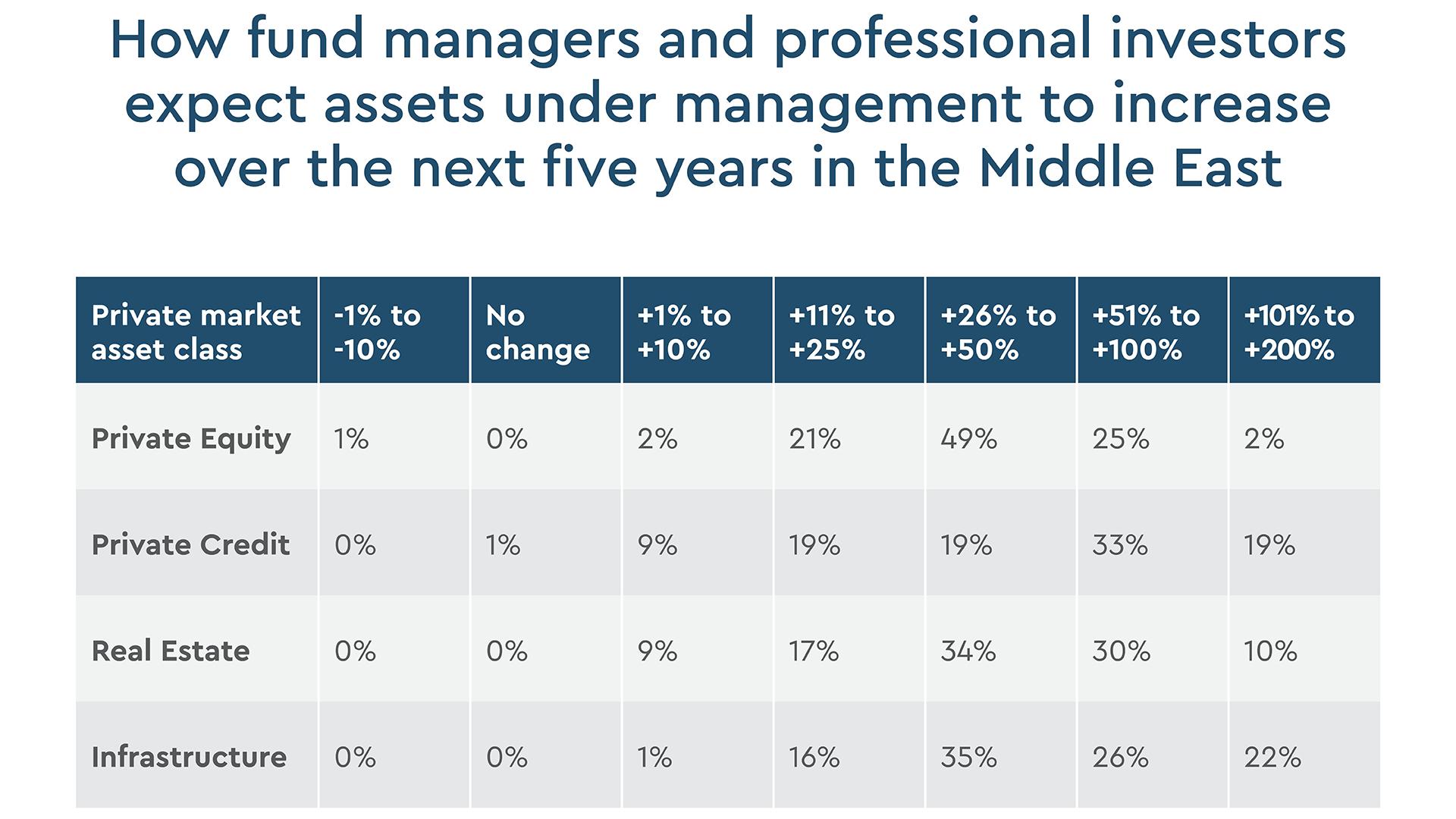

The view of fund managers and investment professionals in the Middle East

Middle Eastern private markets assets under management hit a record $73 billion at the end of 2025, up from $64 billion in 2024.

An Ocorian survey** of fund managers and investment professionals based in the Middle East who collectively manage $2.88 trillion in assets reveals that almost all expect strong growth in all private markets sectors in assets under management in the Middle East over the next five years. All expect growth in real estate and infrastructure and 99% expect growth in private equity and private credit.

Image

Conventional energy and midstream is the sector expected to attract the largest share of institutional private capital in the Middle East over the next five years, followed by financial services and fintech. Almost three-quarters (72%) of those surveyed selected conventional energy and midstream, with 56% choosing financial services and fintech among their top five sectors. Real estate and urban development was chosen by 41% of respondents and infrastructure and transport by 38%, with 34% selecting logistics and industrials.

Ben Hill added: "Given the supportive policy environment, the rapidly expanding and increasingly sophisticated network of capital providers, intermediaries and supporting market structures, all coupled with a deep pool of regional riches and inflows of international wealth and talent, there is no reason why private assets should not grow significantly over the next five years. Indeed, we think the expectations uncovered in our survey are likely to be exceeded.

“The region is playing catch up and in our view its assets under management can comfortably double over the next five years across the four main asset classes.”

*Please see notes on research Methodology

** In January 2026 Ocorian commissioned independent research company PureProfile to interview 100 Middle East-based fund managers and professional investors in Saudi Arabia, United Arab Emirates, Bahrain, Qatar, Oman and Kuwait, working for organisations with total assets under management of $2.88 trillion

Methodology

Ocorian commissioned 5iresearch to produce the Global Asset Monitor which considers eight main asset classes that make up the vast bulk of the world’s assets. Four of these are in public markets, namely listed equities and three categories of listed bonds (corporate, sovereign, and other which include municipal and agency bonds). The other four are in private markets, namely funds investing in private equity, private debt, infrastructure and real estate. We recognise there are other kinds of assets out there in the world, such as residential and commercial property, commodities, art and so on. But we have chosen ours to represent the easily investable universe: investors can buy public assets on exchanges and they can participate in private markets via funds.

Basic private market data is sourced from Preqin unless otherwise stated, but since this data is only available infrequently and with considerable time lags, we have modelled an up-to-date valuation for private assets by looking at the change in value of relevant public markets since the last Preqin update was released and adjusting the values accordingly. These ‘nowcasts’ are intended only to provide a guide to recent developments.

Public market data is sourced mainly from Factset. Data was captured in January 2026. The equities time series looks at the largest 2,250 companies in the world today and how their market capitalisations have evolved over time. These companies represent 85% of global market capitalisation so we have scaled up by the remaining 15% to show the full global equity market value in each year. To measure the size of the bond markets we have considered both the market value and the face value in each country (and sector in the case of corporate bonds) each year – sourced from Factset. Where data limitations impact the sovereign results, we have derived our figures by using general government debt levels as a proxy for the bond market. All data is converted to USD at prevailing spot rates. Currency fluctuations may therefore make an impact in the short term, but over the long-term the effect of exchange rates tends to even out almost entirely at the global level. No account has been taken of inflation.

Related Items

View all