MAS proposes changes to Product Highlights Sheet and the Complex Products Framework

The MAS has proposed several practical changes to its Product Highlights Sheet following a behavioural study to make it useful for retail investors. It also realizes that the widely used terms ‘Excluded Investment Products’ and ‘Specified Investment Products’ don’t make intuitive sense for investors. The regulator has therefore decided to call it “non-complex” and “complex” products respectively.

On 1 July 2025, the MAS issued a consultation paper (CP) titled ‘Consultation Paper on Enhancements to Product Highlights Sheet (PHS) Requirements and the Complex Products Framework’ to enhance the PHS and the complex products framework. The proposed enhancements to the PHS aims to capture a more effective summary of offer documents and improve its role in consumers’ financial decision-making. The proposed enhancements to the Complex Products Framework bring upon an intuitive nomenclature for classifying capital markets products and proposes an alternative pathway to qualify consumers to access investment products whilst ensuring that safeguards are not compromised.

The CP comes in two parts as follows.

Part 1: Enhancements to the Product Highlights Sheet (PHS)

Under the Securities and Futures Act (SFA), the PHS needs to be prepared by issuers (or their issue managers) for an offer of capital market products. The PHS is intended to present key features and risks in a clear and concise manner, complementing the offer document, either a Prospectus or an Offer Information Statement, or an Offering Memorandum.

In this regard, following a behavioural science study to explore ways to enhance the usefulness and readability of the PHS, the MAS is proposing enhancements to its PHS template as follows:

Introducing a red colour indicator for complex products

Where the product offered is a complex product, the coloured heading band on the first page of the PHS should be red in colour. Investors will also be encouraged to seek professional advice in relation to the suitability of the product.

‘Question & Answer’ format

The enhanced PHSs will have segment headers in a “question and answer” format, which has proven effective in engaging consumers. Additionally, key product characteristics which were previously dispersed throughout the PHS will be consolidated on the first page under a new segment titled “What are the characteristics of the [product]?”

Use of diagrams

Illustrating fees payable through diagrams proved effective in helping readers grasp the net value of their investment after deductions. Hence, the MAS proposes for the PHS of collective investment schemes (excluding REITs), and Investment-Linked Policies sub-funds to disclose the investment strategy and fees payable through the use of diagrams.

Introductory statements

A set of simplified and standardised introductory statements have been suggested to help indicate if the product is complex, highlight the purpose of the PHS, and indicate that it should be read carefully in full, together with the relevant offer documents.

Complexity disclosure statements

The regulator offers to include standardised statements under the suitability section of the PHS, to bring to consumers’ attention to the implication of a product’s complexity classification vis-a-vis their own investment knowledge. The statement will be flagged out in a cautionary warning box to alert consumers to pay closer attention and seek advice if needed.

Certain financial ratios

The CP indicates that firms may be required to disclose financial ratios for the PHSs of Equity Securities, Hybrid Instruments, Debt Securities, Post-Seasoning, and Exempt Bonds. Issuers are to determine the financial ratios to be disclosed, and each financial ratio is to be accompanied by a short description to help retail investors interpret the financial ratios and explain their relevance.

Issuer’s asset and revenue profile

The MAS proposes to require the disclosure of an issuer’s (and guarantor’s, if applicable) asset and revenue profile in the PHSs of Equity Securities, Hybrid Instruments and Debt Securities that are made in or accompanied by a prospectus. This would offer retail investors a concise overview of the issuer’s (or guarantor’s) sectoral and geographical presence, and their corresponding market exposure.

Business strategies and issuer plans

The CP also discusses the potential removal of the existing requirement of disclosing “business strategies and future plans of issuer” from the Hybrid Instruments PHS.

Part II: Review of the complex products framework

The complex products framework was introduced in 2012 to aid retail investors to better understand the features and risks of a complex product before transacting in it. The MAS understands that retail investors face two key challenges. First, they may be inundated with investment information and have difficulty identifying the most relevant and crucial information. Second, they may perceive the broad regulatory safeguards that are implemented in the investing process as overly cumbersome and “one size fits all”.

To address these challenges, the MAS proposes the following refinements:

a) Enhanced disclosures that clearly indicate to the investor the complexity of a product, and describe key product features and risks more plainly, so they can make better informed decisions.

b) Streamlined distribution safeguards to be more targeted to the specific type of product, and investor needs.

Enhanced disclosures

Intuitive nomenclature for classifying capital markets products

Capital markets products that are well-established in the market and have features generally understandable by retail investors are defined in MAS Notices as Excluded Investment Products (EIPs). Products that are not EIPs are considered complex products, defined in MAS Notices as Specified Investment Products (SIPs). To help investors more intuitively understand product classification, the MAS suggests that EIPs and SIPs be instead termed as “non-complex” and “complex” products, respectively.

Distributors to clearly disclose that a product is complex

The regulator has proposed that distributing financial institutions perform the following:

Clearly highlight to investors that the product is complex.

Where the PHS is required to be prepared, provide investors with the PHS, or access to the PHS.

Remind investors to review the product information, understand the features of the product, and seek financial advice if needed.

Document that investors have acknowledged the complex nature of the product, verified receipt of the PHS or access to the PHS (where applicable), and the investor’s decision to proceed with the transaction.

Streamlined distribution safeguards

Combining the CKA and CAR

Currently, the Customer Knowledge Assessment (CKA) and the Customer Account Review (CAR) are used for assessing the retail investors’ knowledge and experience when they wish to trade in unlisted and listed SIPs, respectively. Given the similarities in criteria between the CKA and CAR, the MAS proposes to combine the CKA and CAR into a single set of criteria that would be applicable to both listed and unlisted complex products. This will be termed as the CKA.

Product Knowledge Assessment

As the CKA criteria examine the investor’s general investment experience or academic qualifications, meeting the CKA criteria may not always directly translate to the investor’s understanding of the specific features and risks of the complex product he is investing in. The regulator has hence offered to introduce the PKA as an alternative means to evaluate an investor’s knowledge in a complex product. The PKA will comprise questions on the key features and risks of the product type that the investor is investing in.

Financial institutions will be required to offer investors the choice of assessment under the CKA criteria or the PKA. Investors who would not meet the CKA criteria should then be assessed under the PKA.

Removing the requirement for mandatory financial advice (apart from selected clients)

The document propositions removing the requirement for mandatory financial advice even when the investor does not meet the PKA or CKA minimum thresholds. Where an investor is unable to provide the correct answers for the PKA or CKA, financial institutions will be required to provide the relevant information to address the knowledge gap.

They must also communicate to the investor that:

a) The product may not be suitable for them.

b) They should read the offer documents carefully to understand the product features and risks.

c) They are encouraged to seek financial advice (or offer to provide financial advice if licensed to do so) before transacting in the product.

If the investor acknowledges these warnings but still wishes to proceed with the investment, the financial institution may execute the transaction after obtaining the investor’s explicit acknowledgement to proceed despite the warnings, in accordance with its own internal assessment and processes.

However, financial institutions still need to provide mandatory advice to Selected Clients, someone who meets any two of the following criteria and has been assessed not to have adequate investment experience and knowledge:

a) Is 62 years of age or older.

b) Is not proficient in spoken or written English.

c) Has below GCE “O” or “N” level certifications, or equivalent academic qualifications.

Impact on Capital Markets firms (issuers and intermediaries )

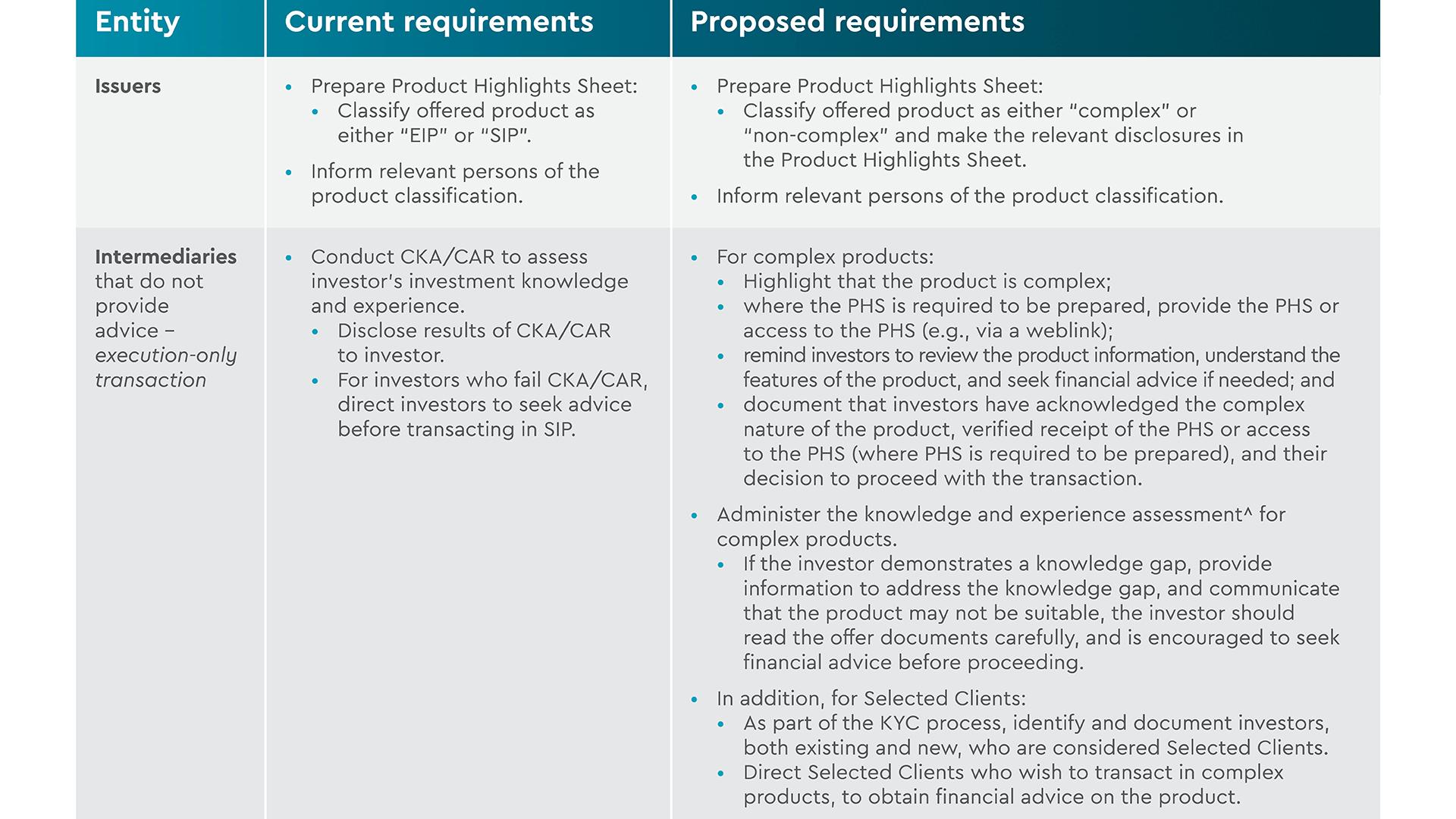

The table below taken from the CP provides a summary of the proposed requirements and their impact on issuers and intermediaries for complex capital markets products.

Image

Given that the proposed measures from MAS are to better protect consumers while to cater to the evolving and diverse investment needs of Singapore retail investors, we think that all, if not most, of the proposals will likely go ahead and be formalised by the MAS.

Issuers and intermediaries should take steps to understand the impact on the PHSs and the way that they qualify consumers to access complex products. Affected firms should put in place implementation plans while the MAS is preparing its response for the CP.

How can Ocorian help?

Our specialist team can help you better understand how these new rules and expectations impact the distribution of capital markets products, and how it will affect your client’s experience.

For smaller firms without their own compliance specialists, we support the management team so they can get on with what they do best. For larger firms we provide specialist skills and can fill resource gaps.

Get in touch if you’d like to discuss the above points in more detail and require support in getting your compliance framework watertight to best manage regulatory risk.

Related Items

View all