A guide to setting up private market funds in Ireland

Ireland has long been used by leading investment firms for the establishment of hedge/UCITS funds for investment purposes. With the evolution of the existing regimes in Ireland to support the full spectrum of alternative investment strategies; many North American asset managers are looking to expand to European fund platforms with new structures for private market type assets.

The US private equity market sees Europe as a vital hedge against their domestic market, and Ireland has become a popular choice for accessing European investments and investors. While Luxembourg' well trodden alternatives system will continue to attract US firms, Ireland's cultural similarities, common law and transparent tax regimes will also likely influence where US managers choose to establish their future structures.

In this article, Stephen Hickey, Eamon Burns and Eileen McCarroll from Ocorian’s Fund Services Team in Ireland delve into the specifics of setting up private market funds in Ireland.

Why is Ireland an attractive jurisdiction to North American asset managers?

Many North American asset managers choose to set up alternative investment funds in Ireland for a few reasons, including:

- EU access and passporting: Ireland is a member of the European Union, which allows funds domiciled there to be easily marketed and sold across the entire EU through the UCITS and AIFMD passport schemes. This is especially attractive to US managers looking to reach European investors.

- Tax advantages: Ireland has a transparent and favourable tax environment for funds. There are no taxes on funds themselves (eg there is no annual subscription tax on funds), and non-Irish resident investors are not subject to Irish taxes (eg stamp duty, capital gains) on their fund gains. Ireland has tax treaties with more than 70 countries, ensuring that income that has been taxed in one country is not taxed again in another.

- Fast fund launch: Ireland's Central Bank fund authorisations are extremely efficient and offers a 24-hour authorisation process for many alternative investment funds such as the Qualified Investor Alternative Investment Fund (QIAIF).

- Strong regulatory environment: Ireland has a well-established and respected regulatory framework for funds, which is attractive to investors.

- Respected stock exchange: The Irish Stock Exchange is widely regarded as one of the leading exchanges in the world for the listing of investment funds.

- English-speaking workforce: Having English as the primary language makes Ireland a good fit for US and other English-speaking asset managers.

- Common law jurisdiction benefits: After Brexit, Ireland is the only remaining English-speaking common law country in the EU, making it an attractive option for UK and North American asset managers seeking continued EU market access.

- Deep-routed funds expertise: Ireland has a highly educated and experienced workforce of over 17,000 people in the financial services and a deep pool of talent. It has a long history of being a successful fund domicile.

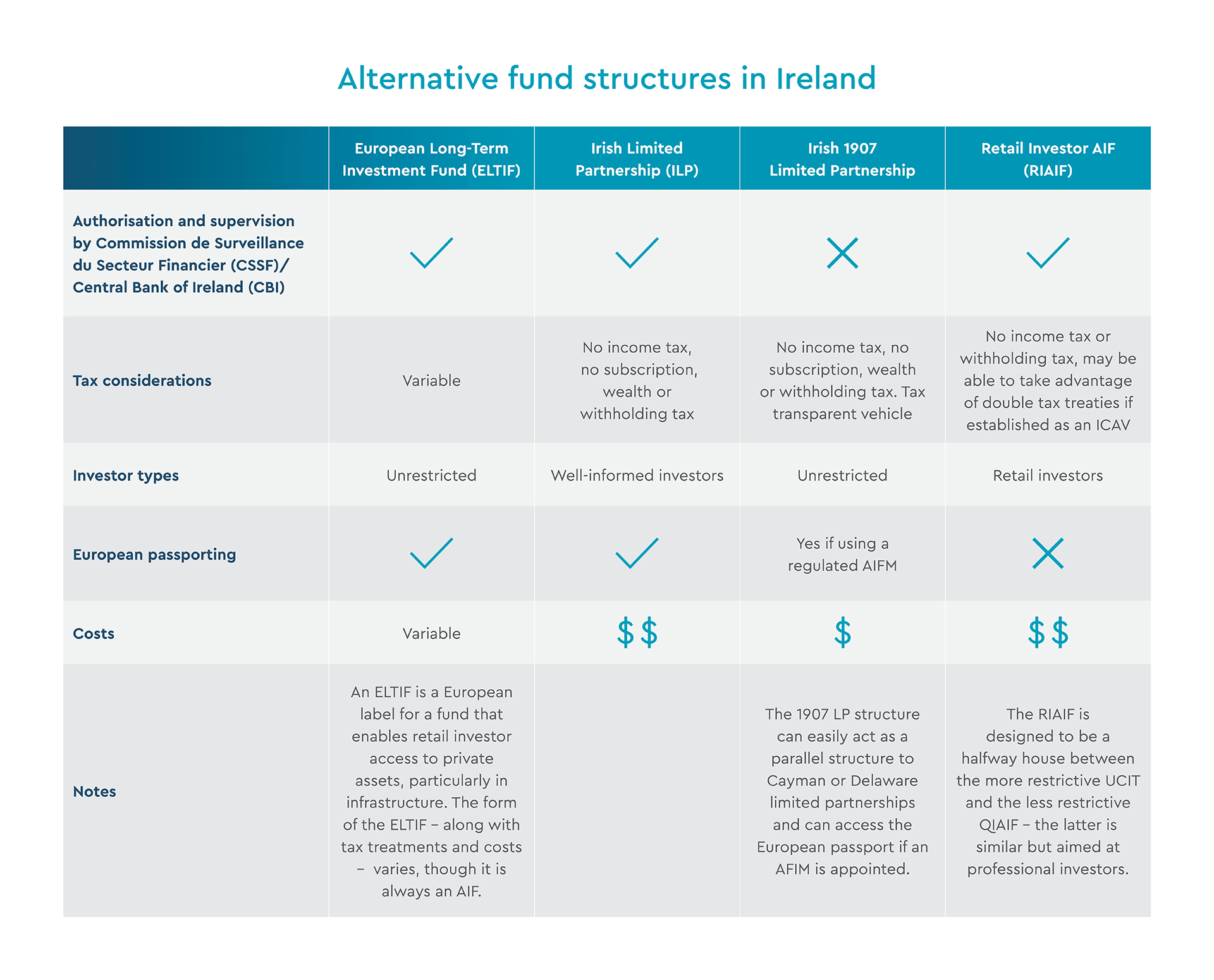

- Variety and flexibility of fund structures: For UCITS funds and AIFs, the Irish Collective Assets Vehicle (ICAV) structure and the Irish Investment Limited Partnership (ILP) are the more utilised structures and are similar to structures that are available in Luxembourg. And finally, for those seeking a completely unregulated vehicle, the 1907 Limited Partnership (LP) is an option. This range of structures ensures Ireland can cater to most investor requirements.

- Modern legal structure: In 2020 Ireland recently the modernised Irish Investment Limited Partnership (ILP) structure, which is specifically designed to be competitive with other popular fund domiciles for private equity and other alternative investments.

These factors all contribute to making Ireland an attractive location for asset managers to domicile their funds.

What fund structures are available for private markets in Ireland?

Governed by the AIFMD (Alternative Investment Fund Managers Directive), AIFs offer more flexibility in terms of assets and investors. They can target a wider range of investment strategies and cater to both professional and non-professional investors.

There are 3 main types of AIFs:

- QIAIF (Qualifying Investor AIF): This is the most popular AIF structure in Ireland for real asset investments. It allows for a wider range of assets and investors compared to UCITS but targets qualified investors only.

- RIAIF (Retail Investor AIF): This structure caters to non-professional investors seeking to invest in alternative assets. It offers more flexibility than UCITS but with stricter regulations compared to QIAIF.

- ELTIF (European Long-Term Investment Fund): The main goal of ELTIFs is to encourage investment in companies and projects that require long-term capital, such as private equity, private debt, real estate and infrastructure developments. ELTIFs are designed to be accessible to a wider range of investors, and were created to bridge the gap between private investments and individual investors by offering a more accessible and regulated way to participate in long-term investment opportunities.

How should you go about choosing the right structure for your business?

Choosing the right fund structure for an Irish investment vehicle depends on several factors. Legal and tax advisors are typically recommended to navigate these complexities. Some key considerations include:

- Investor type and location: The structure should cater to the specific investor profile, whether they are retail, professional, or qualified investors. Additionally, their location plays a role, as some structures allow for easier pan-European marketing and distribution.

- Asset class: The type of assets the fund invests in can influence the choice of structure. Traditionally, Ireland attracted a lot of US hedge funds due to factors like shared language, legal system, and time zone. However, the Irish government has recognised the potential of the US private markets and has made significant efforts to compete with Luxembourg, a dominant player in this area. Now managers with real estate investments typically favour the ICAV structure for their funds, whereas the ILP is more commonly used for private equity and venture capital investments.

- Asset location: Where the underlying assets are physically located can also be a factor in determining the most suitable structure. Compared to Luxembourg, Ireland now boasts a larger pool of service providers and talent to cater to the needs of private market funds. Additionally, some believe that Luxembourg might be reaching capacity in terms of servicing this growing sector, potentially making Ireland a more attractive option.

What regulations should you consider?

For US asset managers considering establishing a presence in Ireland, there are several regulatory considerations to keep in mind:

Manager regulation:

Managers looking to carry out regulated activities in Ireland and set up a physical office in Ireland will require regulatory authorisation from the Central Bank of Ireland (CBI). Alternatively, if opting to utilise a third-party manager, the regulatory status of the manager in their home country will influence the setup approach.

Delegation of investment management:

In terms of delegation of investment management, the CBI recognises the US Securities and Exchange Commission (SEC) as a competent authority. This recognition allows a fund launched in Ireland, perhaps by a third-party AIFM like Ocorian, to delegate its investment management functions to a US manager regulated by the SEC.

However, if the manager is only an advisor and not regulated by the SEC as an investment firm, Ocorian would need to act as the investment manager, making investment decisions and appointing the US entity as an advisor rather than a delegate.

Nuances for different asset classes:

This distinction is crucial in sectors like real estate, private equity, and venture capital (VC), where many US managers operate primarily as advisors due to less stringent regulations in the US. In such cases, when a European AIFM appoints such an advisor as its investment manager, different agreements and regulatory authorisations are required in Ireland.

For hedge funds and public markets, where large US managers are typically SEC-regulated, the CBI allows these managers to delegate investment management. Here, an Irish AIFM may still act as the legal manager while delegating investment decisions.

Additionally, it's important to note that Ocorian offers delegated advisory services from its offices in Dublin and Luxembourg, enhancing the support available to US managers.

Nuance of 24 hour authorisation process

While the 24-hour authorisation for managers is certainly an attractive feature, it's important to understand the process behind it. This expedited authorisation is granted by the Central Bank assuming all the preparatory work has been completed beforehand.

In reality, getting all the necessary documentation and application forms in perfect order typically takes between 10 and 16 weeks. The key takeaway is that the 24-hour approval hinges on meticulous preparation upfront to ensure a complete and flawless application.

Who can establish funds in Ireland?

In Ireland, a variety of entities are eligible to establish investment funds, each catering to different needs and structures within the financial landscape. These include:

- Management companies: These entities are responsible for the day-to-day operations of investment funds. Their duties encompass a wide range of functions including responsibility for portfolio management and risk management.

- Alternative Investment Fund Managers (AIFMs): AIFMs are specialised firms that are authorised by financial regulators to manage alternative investment funds (AIFs). Unlike traditional mutual funds, AIFs can invest in a broader array of assets, offering a more diverse investment portfolio.

- Super Management Companies (SuperManCos): These are essentially management companies that hold an authorisation from the CBI to manage both UCITS funds and AIFs.

- Self-Managed Investment Companies (SMICs): SMICs are investment funds that opt to manage their own operations directly, without the involvement of a separate management company. This model is particularly appealing to smaller funds or sophisticated investors who prefer direct control over their investment decisions and strategies. However given the introduction of the CBI’s CP86 which mandates certain resourcing requirements, these have become less popular.

- Law firms: Law firms with a global registration services department, can also establish funds. These firms must have a power of attorney from the AIFM or Management Company, authorising them to act on behalf of the fund.

What is required to get a fund established/approved in Ireland?

Establishing and gaining approval for a fund in Ireland involves a comprehensive process that requires the coordination of various key parties and the preparation of numerous documents and agreements. Here’s a detailed checklist to guide you through the necessary steps:

Appointment of key parties

To ensure proper management and compliance, the following parties must be appointed:

- Alternative Investment Fund Manager (AIFM): Oversees the fund's operations and compliance with regulatory requirements and in the absence of an appointed investment manager will act as portfolio manager.

- Depositary: Responsible for the safekeeping of the fund's assets.

- Fund administrator: Manages the day-to-day operations and administration of the fund.

- Transfer agent: Handles the issuance and redemption of the fund’s shares.

- Investment manager/sub-investment manager: Makes investment decisions on behalf of the fund.

- Prime broker (if applicable – only for trading funds): Provides services like lending, leverage, and clearing.

- Legal advisor: Ensures the fund complies with legal and regulatory requirements.

- Auditor: Conducts the fund’s financial audits.

- Company secretary: Manages governance and compliance matters.

- Money Laundering Reporting Officer (MLRO): Ensures compliance with anti-money laundering regulations.

- Directors: Oversee the fund’s operations and ensure it meets its governance obligations.

AIF setup list - material contracts

The establishment of a fund requires the drafting and signing of several critical contracts:

- AIFM Agreement

- Investment Management Agreement

- Depositary Agreement

- Administrative Agreement

- Transfer Agency Agreement

- Investment Advisory Agreement

- Distribution/Paying Agent Agreement

- Prime Broker Agreement (if applicable -only for trading funds)

- Sub-Depositary Agreement

Required documents

A set of specific documents must be prepared and submitted for regulatory approval:

- Directors’ letter of application: Formal request to establish the fund.

- Completed application form: Must be filled out with details about the fund.

- Prospectus/private placement memorandum plus any supplements: Detailed information about the fund’s investment objectives, strategies, and risks.

- Constitutional documents of the fund: Includes articles of association and other foundational documents.

- Certificate of incorporation: Official document that forms the legal entity of the fund.

Tax registration

Proper tax registration is crucial for the fund’s operation:

- Corporation tax registration

- VAT registration

- Director/Employee/PAYE registration

Each of these steps involves detailed preparation and coordination with various financial, legal, and regulatory bodies. Ensuring that all these elements are correctly handled is essential for the smooth approval and operation of a fund in Ireland.

Ocorian Fund Services in Ireland

At Ocorian we have extensive experience supporting North American and non European fund managers with setting up alternative investment funds in Europe for the first time and administering funds throughout their lifecycle.

We have teams across seven jurisdictions in Europe that provide a high touch, technology first approach combined with local expertise. We offer a full service offering from fund set up and administration through to fund accounting, AIFM, investor services and depositary.

- Fast and efficient set up of funds in Europe

- Teams based in the UK, Jersey, Guernsey, Ireland, The Netherlands and Luxembourg

- AIFMs in Ireland and Luxembourg

- Expertise in administering vehicles parallel to existing US or Cayman structures

- Jurisdiction agnostic

- Full service provider

Our business development team in the US will be happy to discuss your European requirements and guide you through the process. Contact us for more information.

Download our free guide: Raising Capital in Europe

Fill out the form below to receive your copy:

Related Items

View all