Cross-border European deals powering private credit growth

90% of private credit professionals say cross-border direct lending deals are increasing

Technology is predicted to see the most growth in direct lending in Europe with the UK and Ireland expected to see the highest volume of new loans in the year ahead

Cross-border European deals are contributing to strong growth in private credit compared with last year and the previous three years, new research* from Nordic Trustee, part of global capital markets services provider Ocorian, shows.

Around 90% of private credit professionals surveyed across the UK & Ireland, Germany, Switzerland, Benelux, the Nordics and Eastern Europe say cross border direct lending deals are increasing in Europe with 37% saying they are increasing significantly.

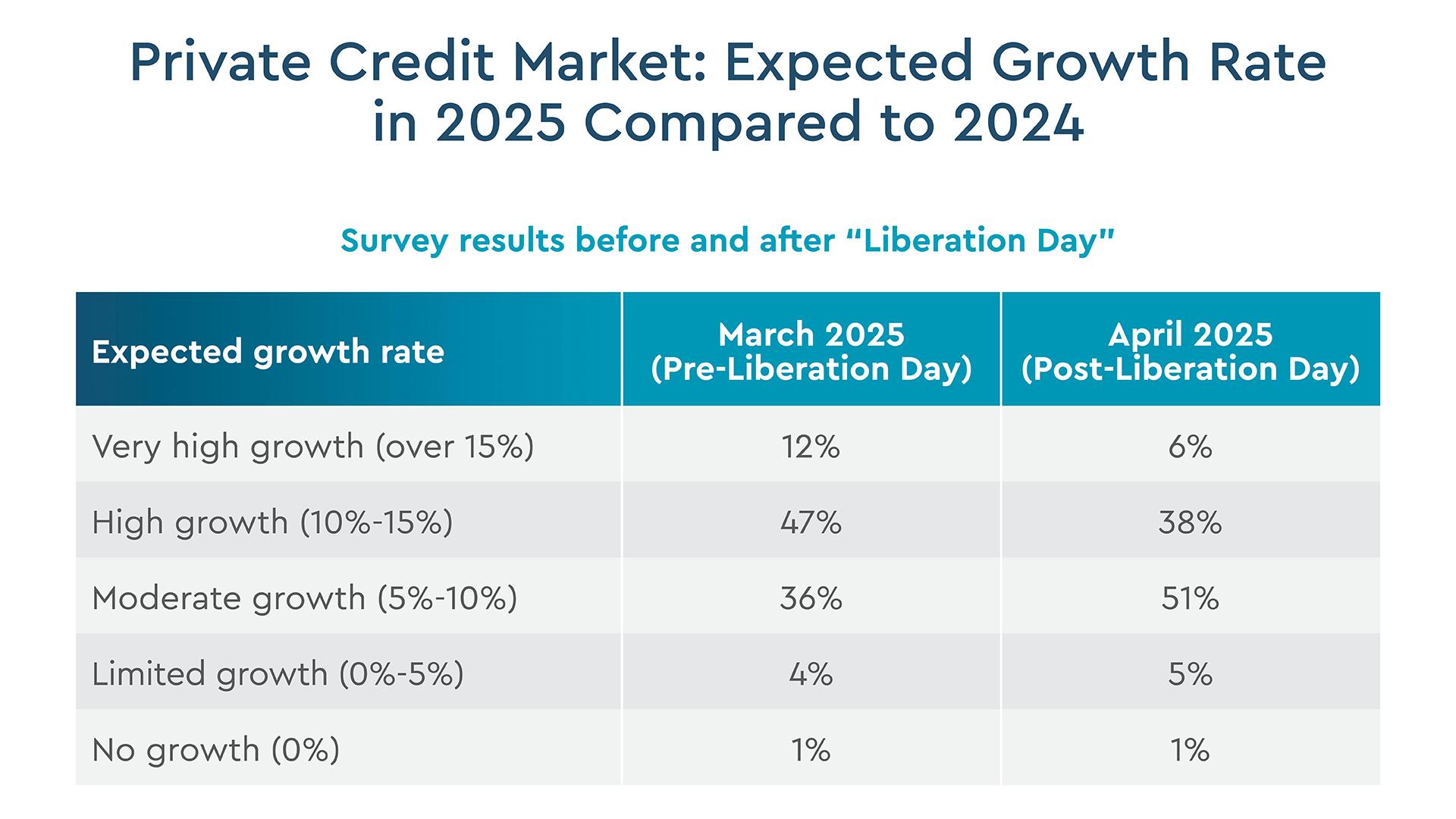

The original study with professionals working across private credit and debt fund management, investing in private debt, private equity and corporates using private credit as a source of funding and for debt advisory firms, carried out in March shows they are predicting strong growth this year. The study** was re-run again a few weeks after “Liberation Day” to see if the recent volatility and change in capital market sentiment had affected respondents’ growth expectations for the year ahead.

The answer, maybe surprisingly, was that private credit investors do not seem particularly concerned. Prior to “liberation day” respondents were expecting 11% growth this year and when the research was re-run in light of the market unrest their growth expectation was marginally reduced to 9.9% for 2025.

In March 59% said they expected high growth of between 10% and 15% or very high growth of more than 15% in the private credit market this year compared to 44% when asked in April. More than half (51%) asked in April said they expected moderate growth in the private credit market this year compared to 2024.

Image

The technology sector is expected to see the most growth in direct lending in Europe in the next three to five years ahead of real estate and energy and renewables. The infrastructure and healthcare sectors are ranked fourth and fifth ahead of consumer goods and project financing.

The UK and Ireland was ranked the European region expected to see the highest volume of new private credit loans in the next 12 months when professionals were asked to rank their top three regions. The DACH region was ranked second ahead of Benelux, the Nordics, Eastern Europe, France, Italy and Spain and Portugal.

It was a similar story on the highest growth percentage of new loans with the UK and Ireland, DACH, Benelux and the Nordics ranked in the top four. Italy however was ranked last behind Spain and Portugal.

The biggest drivers of direct lending growth, according to the research, is increased demand for capital, which was ranked first when professionals were asked to rank their top three. Falling interest rates, lack of appetite from traditional bank lending and uncompetitive terms were ranked second and third.

M&A activity, regulatory change and increased risk appetite and more competitive terms from private credit lenders is also driving growth in the next three to five years.

Private equity is expected to contribute to growth too, the study found, with 83% questioned saying they expect the trend of private equity firms relying on private credit to help fund LBOs and M&A activity instead of public markets to increase.

Cato Holmsen, CEO at Nordic Trustee, said: “Cross-border direct lending deals are becoming increasingly important in Europe and that is highlighted by our study, which forecasts strong growth this year compared with last year. While tariff wars have ratcheted up and de-escalated, stock and bond markets have corrected and rebounded, and forecasts for economic growth have changed with dizzying speed, the private credit market has stoically looked beyond all this turmoil”.

“The key drivers of direct lending growth over the next three to five years are expected to be rising demand for private capital and falling interest rates as well as traditional banks not competing or wanting to compete.”

“Growing use by private equity of private credit to fund M&A and buyouts is also making a major contribution highlighting the need for expertise and experience in the market.”

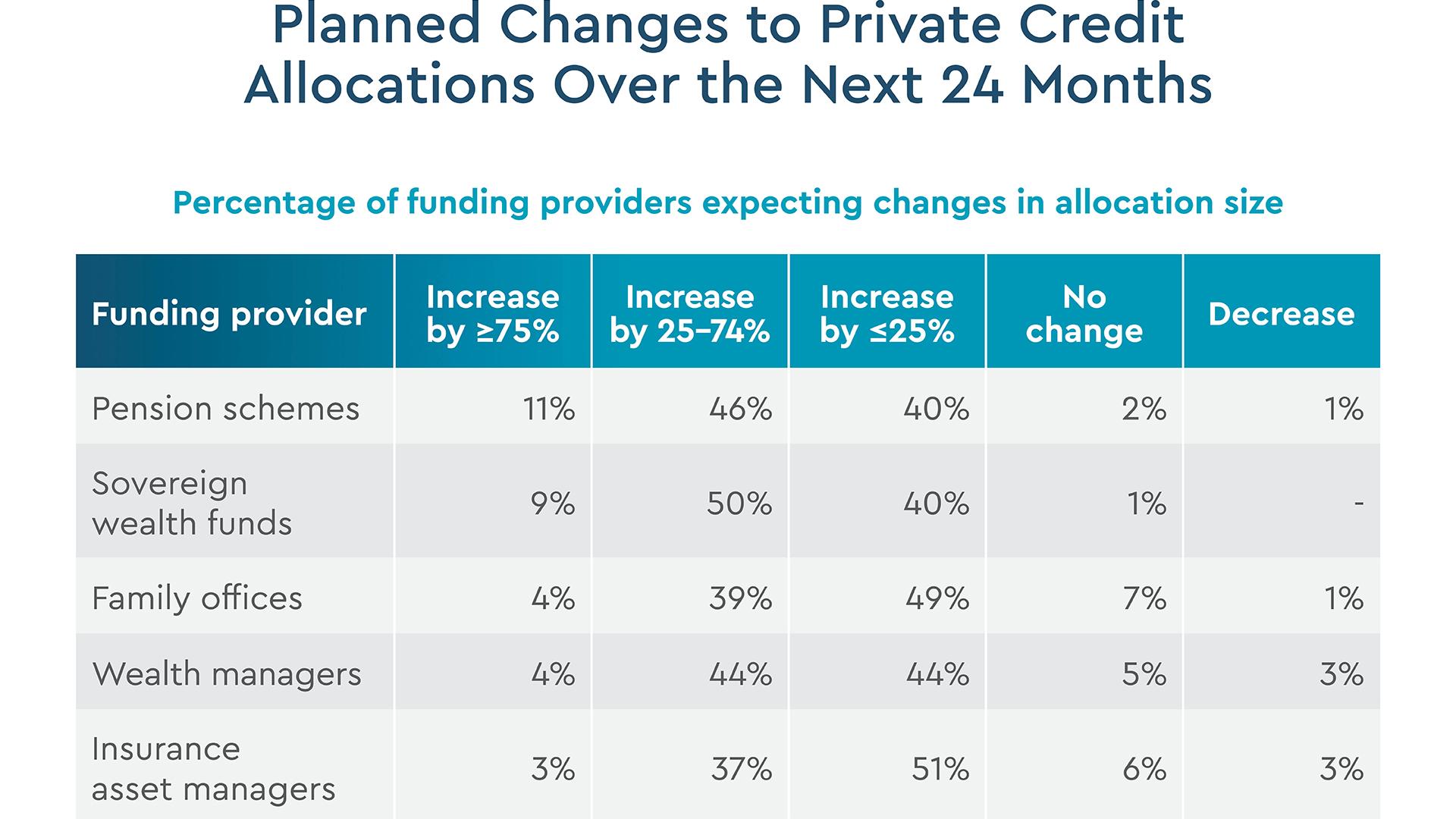

The table below shows allocations to private credit are expected to increase across different funding providers all expected to substantially increase allocations over the next two years.

Image

With over 30 years’ expertise in the bond market and a track record of facilitating 14,000 bond transactions, Nordic Trustee brings an unparalleled depth of knowledge to support bond issuances in the UK and Europe.

It differentiates itself through its proprietary technology, extensive restructuring expertise which includes more than 450 restructurings and 2,000 noteholder meetings, and a problem-solving approach that streamlines complex transactions for issuers and investors alike. Nordic Trustee is committed to delivering best-in-class trustee services tailored to the needs of issuers, investors, and intermediaries.

* In March 2025 Ocorian commissioned independent research company PureProfile to interview 210 private credit professionals working across private credit and debt fund management, investing in private debt, private equity using private credit, borrowers using private credit as a source of funding and debt advisory. Respondents were based in the UK and Ireland, Germany, Switzerland, Benelux, the Nordics and Eastern Europe

** In April 2025 Ocorian commissioned independent research company PureProfile to interview 210 private credit professionals working across private credit and debt fund management, investing in private debt, private equity using private credit, borrowers using private credit as a source of funding and debt advisory. Respondents were based in the UK and Ireland, Germany, Switzerland, Benelux, the Nordics and Eastern Europe

Related Items

View all