What you need to know about the DFSA's client asset regime

On 14 March 2025, the DFSA released a Feedback Statement in response to CP160 on proposed changes to the client asset regime. Further clarification has been issued by the DFSA on 24 June 2025, taking an FAQ format to provide further detail on the regime changes. Firms now have until 1 January 2026 to implement changes ensuring they remain compliant.

The Frequently Asked Questions (FAQ) which came alongside the updated regime highlighted a group of areas focused on improving investor protection and ensuring the industry is prepared to deal with any risks.

Here are the main points from the FAQ to keep front of mind.

Controlling client assets

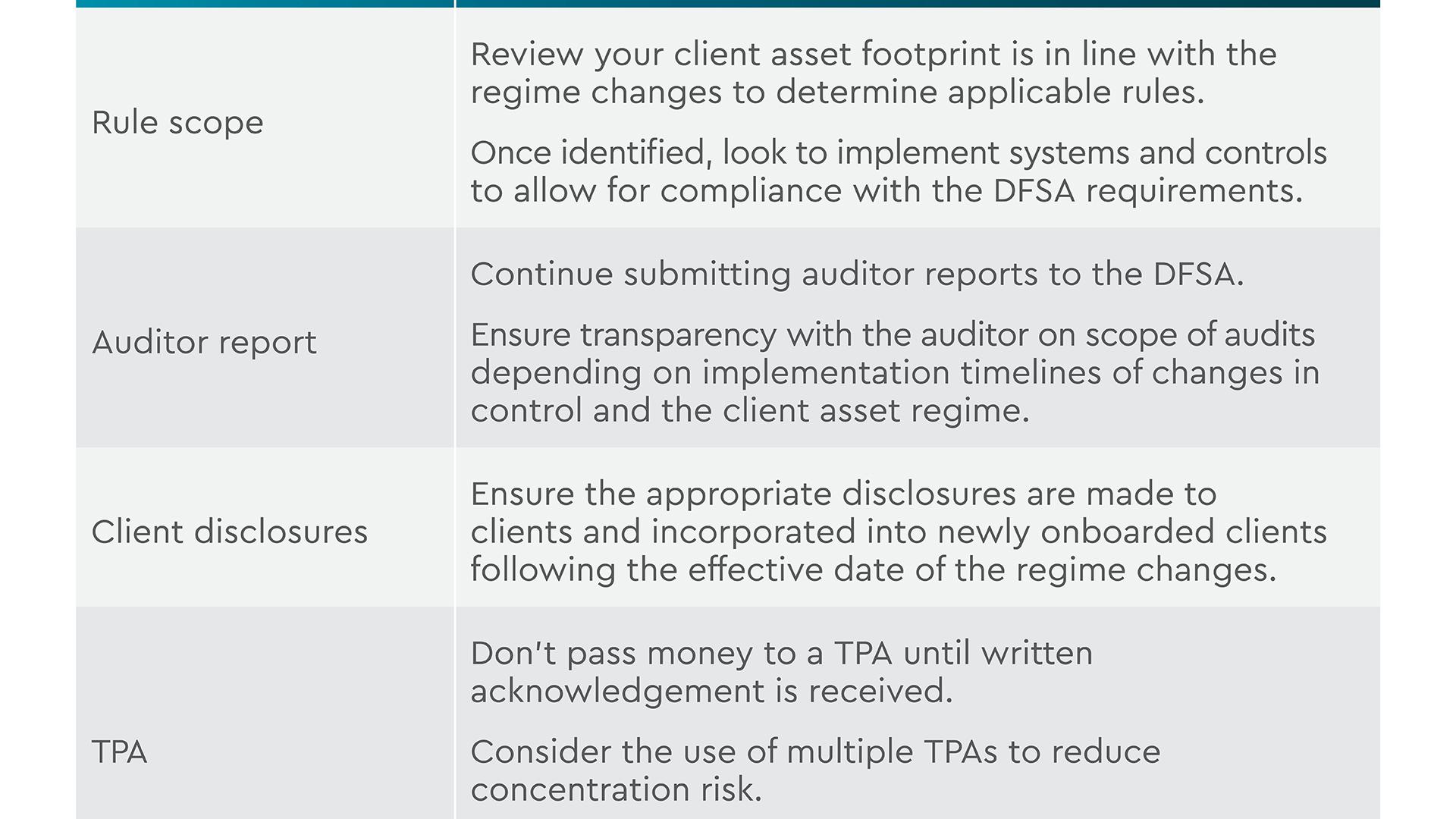

Authorised firms with permission to control client assets will only be required to comply with specific rules within COB App 5 and 6.

Identify which rules apply to your client asset footprint and implement systems and controls to ensure compliance.

Auditor report submissions

Firms with a year-end of 1 January 2026 are required to provide dual reporting, covering both the period of compliance prior to implementation and compliance with the regime changes.

Continue submitting your audit reports prior to the effective date to make sure you’re keeping your compliance records on track; this includes both the Client Money Auditor’s Report and the Report on the Auditor’s findings.

Written acknowledgement timing

Make sure you gain written acknowledgement from a Third-Party Agent (TPA) before any money is passed to the TPA.

Reconciliation frequency

Reconciliations should be performed at a minimum frequency of monthly.

Consider whether a more frequent approach is required based on the volume, size, and value of transactions.

Client reporting and disclosures

Reporting frequency to clients remains unchanged, with firms advised to continue operating per COB A6.8.

Clients should receive disclosure of any relevant aspects of the insolvency regime in the TPA’s jurisdiction. This should be tailored to how their assets are held and would be treated.

It’s also important to capture the existence and scope of depositor guarantee schemes in the TPA’s jurisdiction.

Third-party agent suitability assessment

Firms are required to maintain a record of the TPA assessment and should be prepared to explain their rationale on decision making to the DFSA. Creditworthiness considerations may include annual reports and accounts, rating agency reports, or any other relevant public information capturing the TPA’s financial position.

Although not mandated, it’s worth considering whether diversification would be beneficial to minimise concentration risk. This may include controls over the limit of client money placed at a TPA.

Crisis preparedness pack

The crisis preparedness pack will support a firm during an insolvency, distribution event, or wind as it contains information to help identify and return client assets.

As insolvency can happen at any time, the pack must be kept updated on an ongoing basis.

Regular stress tests should be performed to test the ability to obtain accurate information in the required timeframes.

Investment management of funds

Firms managing assets of a fund under a delegation or sub-delegation arrangement won’t be in scope of the client asset rules, as these assets will qualify as Fund Property.

If you’re operating under this arrangement and hold the Client Asset endorsement, you can request a removal via the DFSA ePortal.

Where separate business lines are conducted, these should be considered separately for client asset scope.

Actions for DIFC firms ahead of implementation

Image

Looking ahead

With 1 January 2026 marked as the live date, DIFC firms have six months to enhance internal controls, review contracts, and embed processes reflecting the DFSA’s enhanced client asset protections.

How can Ocorian help?

Our team of specialists based across the UK and Dubai have the appropriate expertise of how to ensure you’re complying with the local rules, making sure we find a solution that fits your business and keeps client money safe.

- Implementation of system and control changes to align with the DFSA approach

- Identification and documentation of client asset footprint.

- Creation and review of bespoke policies, procedures and controls

- Remediation of auditor breaches

- Safeguarding health checks

- DFSA endorsement amendments

- Pre-audit preparation and audit support, including auditor report review.

Related Items

View all